From a formation standpoint, the UK remains one of the few jurisdictions where the fast timeline is mostly real. In most countries, incorporation timelines are wrongfully quoted almost every time because they only refer to the moment an application is lodged or approved. The UK is different. The legal setup can move quickly. The challenge sits in the administrative steps that turn a legal shell into a working business.

That distinction matters for growth-stage companies under pressure to show expansion progress in the next board deck. A lodged filing can satisfy optics for a week. It does not create a functioning employer, a payroll-ready entity, or a contracting vehicle.

I co-founded GEOS after spending years in regulated B2B environments and after seeing how global expansion still operates in a model that needs some refreshment. At GEOS, we have mapped entity setup and management across 80+ countries. That gives me a practical benchmark. The UK is one of the easiest places for a foreign company to set up a subsidiary in a cheap and fast way. It is also one of the easiest places to underestimate the work that follows.

Why the UK Still Stands Out in 2026

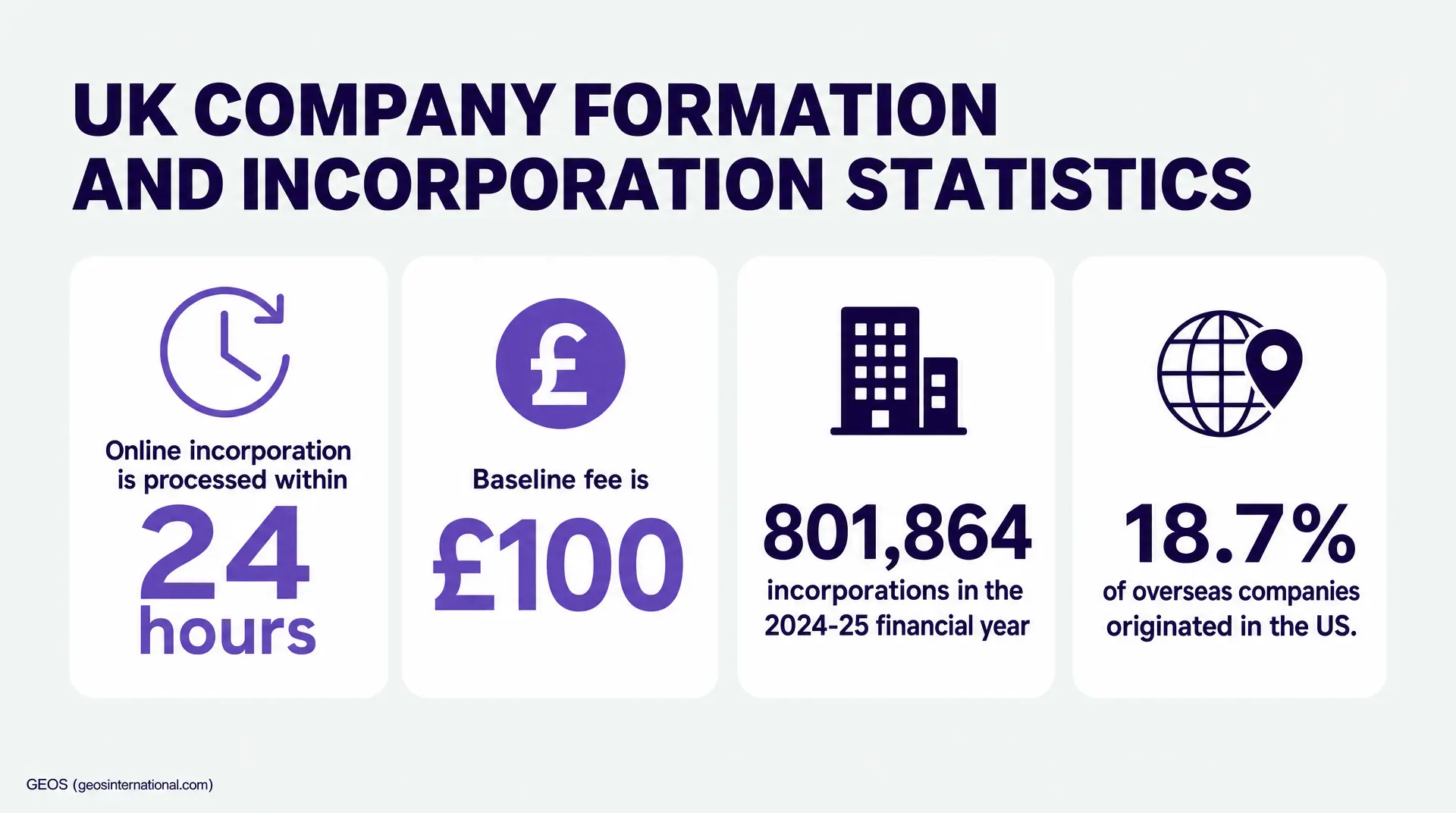

The UK’s formation system is mature, high-volume, and operationally clear. Online incorporation is still usually processed within 24 hours. As of February 2026, the baseline fee for online incorporation is £100. Same-day software filing is £156. That cost profile matters. It keeps the legal formation step accessible for both early and growth-stage companies. It’s important to note that foreign companies entering the the UK would incur additional costs, especially if they prepare for ongoing tax & employment registrations.

The scale of the system matters as well. The UK register now holds 5,427,787 companies. Companies House also recorded 801,864 incorporations in the 2024-25 financial year. Foreign ownership is not unusual in that environment. There were 14,574 overseas companies with a UK establishment as of March 2025, and 18.7% of them originated in the United States.

The first platform dedicated to streamlining entity setup and management.

The First Strategic Question Is Whether the Entity Is Justified

I start with a simple framework. Why the UK, why now, and what infrastructure already exists to support the move. That discipline matters because a foreign subsidiary should be treated as a permanent decision. It should solve more than one problem.

In many cases, the UK entity is justified quickly. The market is straightforward to administer. A local entity can support direct hiring, direct contracting, revenue collection, a local commercial presence, and more control over benefits and equity. Those are real advantages. They often justify going direct earlier in the UK than in harder jurisdictions such as France, Belgium, Mexico, or India.

I do not think every company should incorporate on day one. There are usually five to seven ways to enter a market. If the only goal is to hire one person or validate early demand, an Employer of Record can still be the right first step. The same is true when the business is testing sales activity and staying below VAT thresholds. Global expansion has a beginning, middle and end. The mistake is assuming the first tool should be the permanent one.

Formed and Operational Are Two Different Milestones

The cleanest way to think about UK company formation is to separate legal incorporation from operationalization of the entity. Founders often focus on the Companies House certificate because it is visible and immediate. Boards like it because it looks like progress. In practice, that certificate only marks the start of the work.

A UK entity is operational when the governance, banking, tax, payroll, and compliance layers are live. In most growth-stage companies, that means the directors are correctly appointed, the identity checks are complete, the registered office is valid, the mail flow is controlled, HMRC registrations are done, payroll is configured, pension duties are set up, and the finance team has a clear path for Corporation Tax and VAT. Until those items are complete, the entity often remains dormant until it needs to become operational.

Governance Now Starts with Identity Verification

The governance point is more important in 2026 than it was a year ago. From 18 November 2025, identity verification became compulsory for new directors and for incorporation itself. Companies House has said roughly 6 to 7 million people will need to verify by mid-November 2026. Director and PSC verification is now a first-order formation workstream. It cannot be left for later.

This is one of the few new administrative hurdles in the UK that can catch a foreign parent off guard. The old view was that UK formation was almost frictionless. The new view should be that formation is still fast, but the governance layer now needs active ownership from day one.

Registered Office and Mail Flow Still Matter

The registered office is another area companies dismiss too quickly. Since March 2024, every company must maintain an appropriate registered office address, and a PO Box cannot be used as the registered office. A registered email address is also mandatory.

This matters because parts of the UK process still rely on physical correspondence. Codes arrive by post. Notices arrive by post. That means mail flow is part of compliance. If the address is poorly managed, or if no one is clearly responsible for reviewing incoming notices, a simple administrative issue can turn into a good-standing problem.

HMRC, PAYE, Payroll, and Tax Need Parallel Planning

The HMRC sequence is usually where the gap between formed and operational becomes obvious. PAYE registration must be completed before the first payday. HMRC also will not accept the registration more than two months before paying staff. That narrow window matters for companies trying to time offers, onboarding, and payroll in parallel.

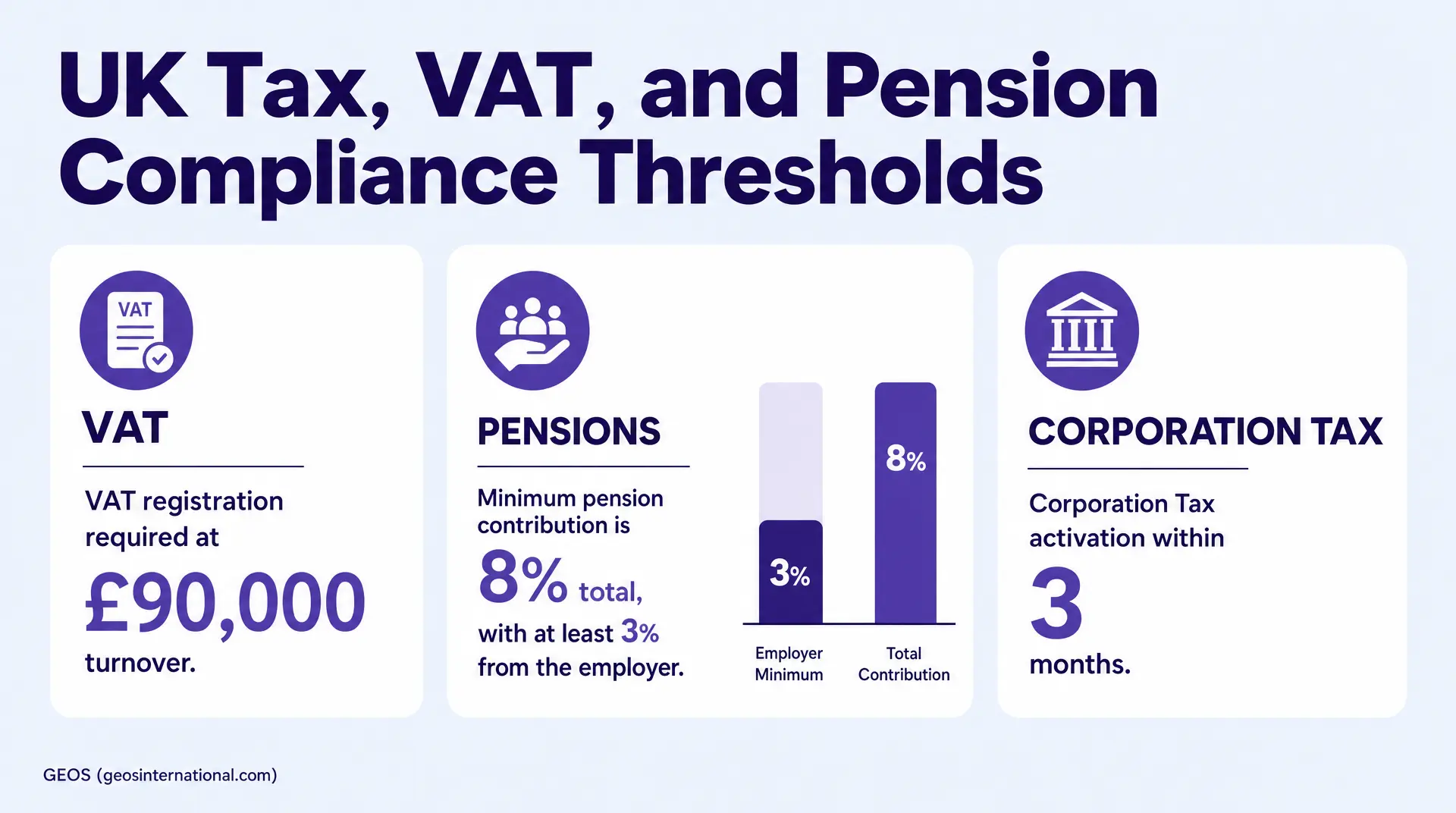

Payroll reporting then has to be submitted on or before the first payday. Corporation Tax has its own activation logic. A company must tell HMRC within three months of becoming active for Corporation Tax purposes. Early planning or contract negotiation may not count as active trading, but the transition into activity still needs to be tracked carefully.

VAT also needs early attention. A business must register once taxable turnover exceeds £90,000. For businesses based outside the UK, the requirement can arrive earlier because UK supplies may trigger registration regardless of turnover. For e-commerce and services companies, this is often the point where the UK setup stops being only a hiring decision and starts becoming a broader finance and tax workstream.

Pension Setup Is Part of the Infrastructure

Pensions are not a minor payroll setting. They are part of the employment infrastructure. Automatic enrolment requires minimum contributions of 8% of staff earnings, with at least 3% paid by the employer. Deducted employee amounts generally need to be remitted by the 22nd day of the following month.

In practical terms, a UK setup is only clean when payroll, pension, and tax are designed together. If those streams are handled in isolation, the business usually ends up playing catch up in terms of what was missed.

Banking Is Often the Real Bottleneck

In the UK, the legal filing is rarely the slowest part. Banking is more often the point where the timeline stretches.

Official UK guidance says opening a business bank account can take 4 weeks to 3 months. Foreign-owned entities often face added identity checks, sanctions screening, and requests tied to foreign directors or shareholders. This is where aggressive timelines lose credibility. The entity exists, but the infrastructure needed to use it is still pending.

My view is practical. If a fintech account is sufficient, it is usually the fastest path. Official guidance also notes that a digital account is usually easier and quicker to open than a traditional high-street account and can work as a short-term arrangement. When a client needs a legacy bank for treasury, contracting, or internal policy reasons, I prefer to surface that requirement at the start. In some cases, GEOS will appoint a temporary nominee director for three to four months to help establish the account and then transfer control back. That is a targeted operational solution. It is not a long-term governance model.

AI Can Help, but the Process Remains Partly Manual

There is a lot of noise around AI automating global compliance. The UK is one of the few countries where parts of that thesis are directionally right. The portals are more digital. The filing steps are cleaner. The information is easier to work with than in most jurisdictions.

Even so, the process still has manual points that matter. Director verification still requires the right people to act. Physical mail still matters. Authority needs to be assigned correctly for tax and payroll registrations. When companies try to push the whole process through a generic tool, the first failure is usually practical. A registration is misconfigured. The wrong person is given authority. A code is missed.

At GEOS, we use technology as an enabler. It maps the process. It centralizes documents. It makes the work visible. Our AI layer helps clients retrieve information and navigate their own entity footprint. It does not replace the local, manual, last-mile tasks that remain AI resistant for a while.

The UK Has One of the Lowest EOR-to-Entity Crossover Points

I spent enough time on the EOR side of the market to have a balanced view here. EOR is a very effective launch tool. It solves a real problem. It can be the best option for the first one or two hires in a new country.

The UK changes the math quickly because it is easy to set up and maintain. In my view, the breakeven point is low. I start looking at the move very early, often around three to six employees. By the time a company is sitting on 10 UK EOR employees, the argument for direct ownership is usually strong.

The financial side is straightforward. Public pricing from one major provider starts at $499 per employee per month. Another large provider lists $599 per employee per month. At 10 employees, that creates a monthly fee stack near five to six thousand dollars before salaries, taxes, benefits, FX, and add-ons. In a market like the UK, one month of that spend can look very similar to the cost of standing up core local infrastructure.

The control argument is usually even stronger than the cost argument. A direct UK entity gives the company more freedom around pension design, benefits, employment terms, and equity. It also gives the business a clearer local presence when selling into enterprise accounts. EOR liability protection is also narrower than many founders assume. In many contracts, the provider still passes off liability and indemnity to the client for actions driven by the client’s day-to-day control of the employee.

The Vendor Model Still Matters, Even in an Easy Market

Because the UK is fast, the temptation to cheap out on setting up an entity is strong. That is where black-box problems begin. The local lawyer may be fine on the filing itself, but the wider setup often becomes a black box in terms of the steps that need to be taken. The work arrives piecemeal by email or phone calls. Fees appear incrementally. The founder ends up owning the project management without meaning to.

The Big Four version of the problem looks different. There is more coverage and more safety in concept, but the operating model is often bloated and fragmented by region. The client still has to liaise with multiple teams and re-share the same corporate context again and again. I have seen that directly. I have also seen companies choose a better middle path. In one engagement, a business managing four global subsidiaries transferred its compliance operations away from a Big Four provider after we demonstrated a clearer platform and more transparent pricing.

That model becomes much more important once the UK is only the first market. I have also worked with a company that had more than 30 entities and had lost visibility into compliance costs because local firms were billing subsidiaries directly. Untangling years of backdating and work and auditing required a dedicated internal hire working alongside GEOS. That is the operational debt founders should avoid early. Once a footprint spans multiple countries, managing by spreadsheet starts to feel like playing with a blindfold.

My Practical Recommendation for 2026

For founders entering the UK in 2026, the strategic case is strong. The market is fast, mature, and unusually friendly to foreign-owned formation. The legal entity can often be formed in a matter of days, and a fully operational setup can follow quickly when the workstreams are managed in parallel.

The discipline sits in sequencing. First, confirm that the entity solves a real business objective beyond simple hiring. Then treat identity verification, registered office control, HMRC setup, payroll, pensions, banking, and tax as core formation tasks rather than post-launch cleanup. Decide early whether a fintech bank account is sufficient or whether a traditional bank is a hard requirement. Finally, put the entity into a centralized compliance system from day one so the business can keep the lights on from a compliance perspective as the footprint grows.

In the UK, speed is achievable. The companies that benefit most are the ones that pair speed with structure. That is how the market stays cheap and fast without turning into a black box later.

Frequently Asked Questions

At what headcount does relying on a UK EOR destroy operational ROI?

The breakeven point is shockingly low. Once you hit three to six employees, you are bleeding capital. With major EORs charging $599 monthly per head, 10 employees means burning roughly $6,000 monthly – capital better deployed building wholly owned, permanent UK commercial infrastructure.

How do the 2025 Companies House rules block foreign directors from incorporating?

It acts as a hard operational blocker. From 18 November 2025, identity verification is strictly compulsory for new directors before incorporation or appointment. You can no longer lodge the filing and sort out governance later. If your global executives remain unverified, your UK expansion stalls entirely.

Can a newly formed UK subsidiary rely on a digital fintech account for enterprise operations?

Yes, and it is the fastest path to activation. Traditional UK banks take 4 weeks to 3 months for foreign-owner KYC. Official UK guidance explicitly supports using digital fintech accounts as a short-term arrangement, allowing you to run payroll and clear HMRC hurdles immediately.

Does negotiating enterprise contracts activate a newly formed UK subsidiary for Corporation Tax?

No. You can form the legal shell and negotiate safely. Preliminary setup activities, like negotiating enterprise contracts, generally do not make the company active for Corporation Tax. Once official trading begins, however, you have exactly 3 months to notify HMRC and operationalize your tax infrastructure.

When is a foreign-parented UK subsidiary legally required to register for VAT?

Standard UK entities trigger VAT at £90,000 in taxable turnover, but foreign-based businesses must register immediately – regardless of turnover – if they supply goods or services directly to the UK. Do not let this hidden compliance trigger disrupt your early cash flow or client onboarding.