The proposed EU Inc. is one of the most constructive ideas we have seen for cross-border growth in Europe in a long time.

At GEOS, we help companies set up and manage foreign subsidiaries. We spend our time in the practical layer of expansion. That means public notaries, apostilles, share capital, bank KYB, tax registrations, payroll registrations, and the long gaps between each step.

In building GEOS, my team and I spent hundreds of hours mapping what it actually takes to set up and maintain entities in more than 80 countries. We learned quickly that there are no shortcuts. The pain is rarely in the legal theory. It sits in the variance from country to country and in the operational work that follows incorporation.

That is why I see EU Inc as a strong concept. Europe needs a more modern path. The Commission notes that companies still face 27 national legal systems and more than 60 company legal forms, and that setup can take weeks or months. For founders trying to move quickly, that fragmentation creates delay, cost, and a lot of avoidable uncertainty.

A Strong Concept for a Real Scale-Up Problem

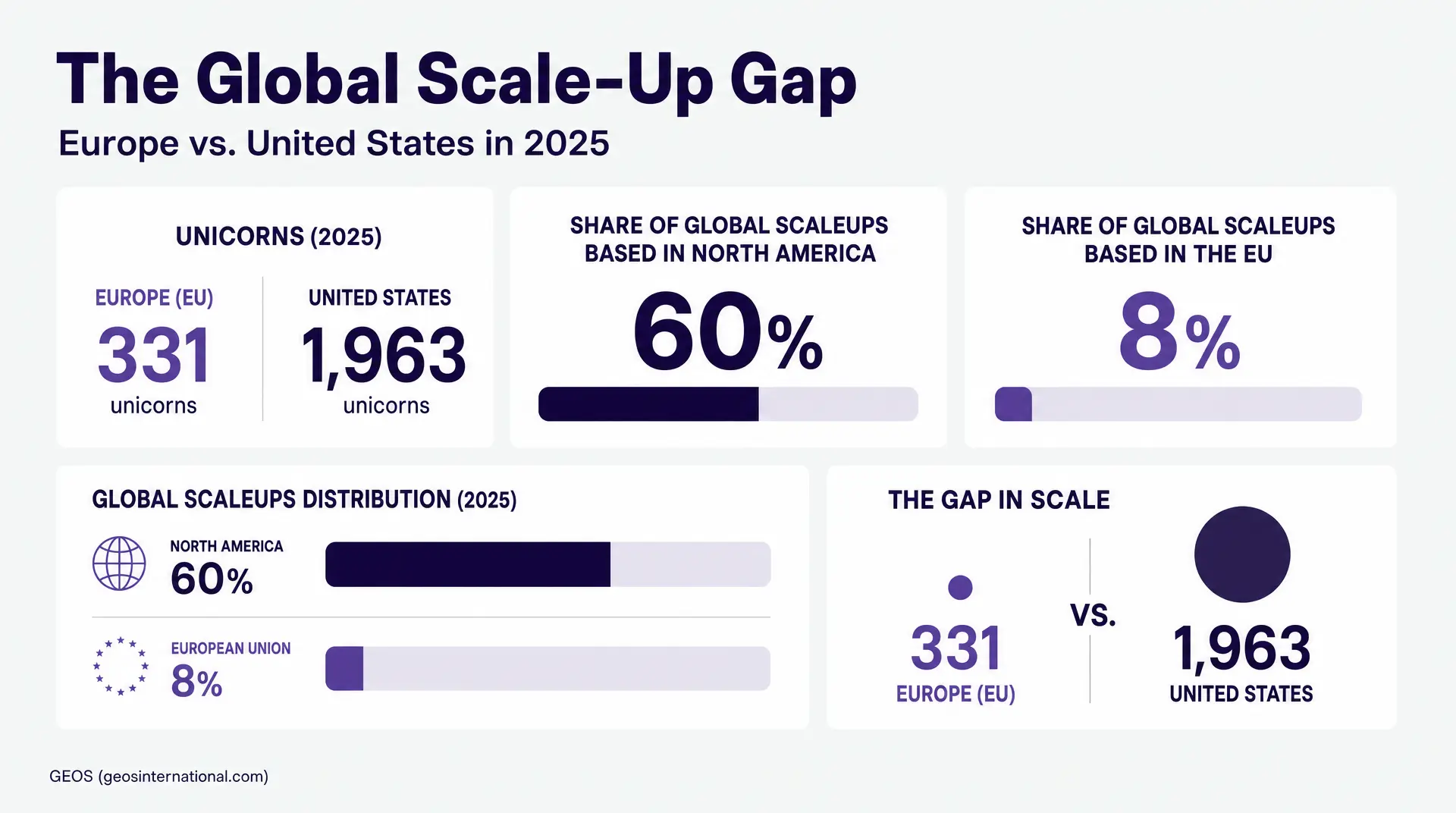

The scale-up rationale behind EU Inc is serious. A Commission communication notes that Europe had 331 unicorns compared with 1,963 in the United States in 2025, despite having more than 40,000 VC-backed tech startups. A separate EU strategy paper says that about 60% of global scaleups are based in North America, versus 8% in the EU, and that the EU accounts for only 5% of global venture capital raised.

Europe does not need another abstract policy discussion. It needs practical tools that make company building easier. EU Inc has the potential to be one of those tools.

The Commission estimates €328 million to €440 million in lower administrative burdens over 10 years. Much of that benefit is expected to land with newly formed startups and scaleups. That estimate is credible. In international expansion, the cost is often cumulative. It comes from repeated filings, repeated data entry, repeated document requests, and repeated coordination across local parties.

The structure is also being framed as an optional regime, not a replacement for national company forms. That is the right starting point. It creates room for adoption without forcing every local corporate tradition into one model on day one.

Where the Proposal Stands Today

This is where the conversation needs more discipline. As of 20 May 2026, EU Inc is still in the Preparatory phase in Parliament. The Commission published the legislative proposal on 18 March 2026, but there is no operational company form that a scale-up can use today.

The headline promise is attractive, but it is also specific. The proposal states that registration must be completed within 48 hours and cost no more than €100 when founders use the EU central interface, the harmonized application form, and the EU templates. That is encouraging. It is also a defined process. It is not a general promise that every surrounding operational step disappears.

The proposal goes further than pure incorporation. It tries to apply a once-only principle. Under that approach, company data would move from the business register to the authorities handling tax IDs, VAT IDs, social security, and beneficial ownership registers without being resubmitted. That is smart. It targets a real source of wasted time.

The limit is equally important. The same proposal says provisions touching taxation and employee participation are “not intended to harmonise” those systems. For operators, that sentence matters more than most of the headline coverage. It means the company law wrapper may become simpler while core employment and tax realities remain local.

The political momentum is real. Harmonising company law across 27 legal traditions is still a major undertaking. A serious proposal is now on the table, but there is a long road between that and something a CFO or founder can rely on in live expansion planning.

Incorporation Speed Will Not Remove the Operational Work

The first platform dedicated to streamlining entity setup and management.

This distinction is where many expansion plans break. Legal incorporation and operational readiness are different milestones. In easier markets they can sit close together. In harder markets they are often far apart.

A company can be formed on paper and still remain dormant until the practical infrastructure is in place. That infrastructure is what makes the entity usable. It includes bank setup, tax registrations, payroll registrations, social contribution setup, and local compliance workflows. In some cases it also includes benefits, insurance, import or export registrations, or local vendor support.

This is why incorporation timelines are so often wrongfully quoted. The quoted period may cover only the legal filing window. It may leave out the document collection, the certifications, the local signatures, the bank KYB process, and the last mile tax filings that actually operationalize the entity.

In this space, every step is a surprise when the process is left as a black box in terms of the steps that need to be taken. That is one of the oldest problems in global expansion. The parent company often does not know what it does not know in every jurisdiction. The local provider does know, but the process is presented in fragments.

I have seen this happen in very ordinary ways. A busy executive does not get to a required signature for a week. A UBO resists providing notarized identification because the request feels intrusive, even though it is unavoidable. A local authority or notary asks for one more document after the file was assumed complete. None of that is unusual. It is the normal texture of foreign expansion today.

A faster EU company form would clearly help at the front end. The bigger question is whether the operating path behind that form will be equally clear.

The National Layer Will Still Decide How EU Inc Works in Practice

Banking and KYB Will Remain a Major Hurdle

If I had to pick the most stubborn analog issue in European expansion, I would start with banking. Bank KYB is governed by banks, not by a press release and not by a headline. Those institutions still need to understand ownership, control, risk, and business activity before they onboard a foreign-owned company.

That caution is built into the rules. EU anti-money-laundering requirements obligate banks and similar institutions to verify beneficial owners, understand ownership and control structures, monitor the relationship, and assess the source of funds where needed. That is one reason banking remains slow and variable for foreign-owned entities. EU Inc does not make those obligations disappear.

This matters because a fast shell without a usable bank path is still only a shell. Founders usually feel the delay after incorporation, not before it.

Tax, Payroll, and Employment Remain Country Specific

The same issue shows up in tax and employment. EU VAT is only partly harmonised. The standard rate in each member state must be at least 15%, but the practical obligations still vary by country and by what the company buys or sells. Corporate tax also remains local. EU guidance states that company tax rules are set by national authorities and differ across member states.

Social security follows the same pattern. EU coordination rules help people move across borders, but they do not replace national systems with a single European one. An employer still needs to understand the local contribution framework where the employee sits.

This is why I keep coming back to country-by-country operations. An EU Inc may simplify how a company is formed. It still needs clear answers on how that company hires in Spain, registers payroll in Poland, handles tax in Germany, or manages local compliance in France. Those are the questions that determine whether the entity is useful.

Local Mechanics Still Create Delay

There are also hard local mechanics that a central framework will have to coexist with. In Germany, German company law still requires a traditional GmbH to have €25,000 in share capital, with payment rules that must be satisfied before registration can generally proceed. In Spain, the mercantile registry frequently pauses applications and asks for additional documents. In Poland, post-incorporation steps can require certified signatures such as QPS.

These are not edge cases. They are part of the operating reality. Founders often expect the legal filing itself to be the hardest part. In Europe, the more stubborn delay often appears just after that point.

EU Inc Changes the Math. It Does Not Remove Strategy.

This is especially relevant for companies using an Employer of Record. Every global expansion journey has a beginning, middle and end. EOR often fits the beginning well. It helps companies hire early employees without taking on the full operational lift of a local entity.

That remains true whether EU Inc arrives or not. It is a separate path of global expansion. The move to an entity becomes more compelling once a company has reached critical mass in a market. Monthly EOR fees become more visible. Control becomes more important. Companies want direct employment relationships, local benefits control, better equity administration, and the ability to sign local contracts or show a permanent establishment.

Europe already has examples where EOR is clearly not a permanent answer. In Germany, the Temporary Agency Work Act limits assignment of the same temporary agency worker to the same user undertaking to 18 consecutive months. Rules like that force a strategic decision.

If EU Inc becomes operational and the country-level detail is well executed, it will change the math of when companies flip from EOR to their own entity in Europe. I believe that. I do not think it will remove the need for judgment on timing, headcount, control, tax, or local commercial goals.

The Costly Mistake Is to Wait

For growth-stage companies, the main risk today is waiting for a perfect framework that does not still exist. The opportunity cost is real. Hiring slows down. Revenue plans move to the right. Market share is left on the table.

My bias has always been to execute a B-plus plan today rather than wait for an A-plus plan next week. This is one of those situations. If there is a real business reason to expand into Europe now, the current system is still the one that needs to be planned around.

That does not mean defaulting to an entity in every case. Sometimes an EOR is still the better answer. Sometimes the right move is to validate the market first and incorporate only when there are multiple concrete reasons to justify the cost and lift. The important point is to make that decision using the tools that exist today, not the ones that may exist later.

I would also be careful with any advisory work that presents EU Inc as if the operational roadmap has already been written. At this stage, highly priced readiness work would be premature. The critical questions around country-level operation are still outstanding.

Great Execution Will Decide Whether EU Inc Succeeds

In my view, great execution means Europe has to solve more than formation. The framework needs a predictable operating path into tax, payroll, banking, and ongoing compliance. It also needs to distinguish clearly between a company that is legally incorporated and one that is actually operational.

The compliance layer after setup matters just as much as the setup itself. This industry is still rooted in manual processes. Notices arrive through physical mail. Tasks are divvied up to multiple responsible parties. Parent companies receive updates piecemeal by email or phone calls and end up putting blind trust into local vendors.

Large providers can make this look cleaner than it is. They may sit under one logo and one umbrella, but the service is often fragmented by region. The client still ends up coordinating across multiple teams and restating the same context. That model needs some refreshment.

I have seen the cost of that firsthand. One company managing four global subsidiaries moved away from a Big Four provider after we showed a clearer platform and more transparent pricing. Another company with more than 30 entities had lost visibility into compliance costs because local firms were billing subsidiaries directly. The cleanup involved years of backdating, audit work, and invoice review alongside a dedicated internal hire.

That is what weak execution looks like at scale. Teams end up playing with a blindfold. They do not have one system of record. They do not know which tasks are done, which ones are late, or which costs are justified.

Technology should be an enabler here. It should map the workflow, centralize documents, clarify responsibilities, and show what is due next. It should not pretend to replace the human layer that still exists in local legal, tax, payroll, banking, and government interactions. This part of the market will remain AI resistant for a while. Any serious framework needs to respect that.

Final View

My view on EU Inc is positive. Europe is right to try to make company formation easier. The current system is too fragmented, too slow, and too opaque for the pace at which modern scale-ups need to operate.

The real test now is execution. A 48-hour registration promise will only matter if companies can also bank, hire, run payroll, manage tax, and stay compliant with less friction than they face today. That is the standard the framework will ultimately be judged against.

Until that detail is in place, companies expanding into Europe should move under the rules that exist now and keep a close eye on the framework as it develops. EU Inc is a great concept. It now needs great execution.

Frequently Asked Questions

Will EU Inc let me bypass local banking and KYB delays?

No. Legal incorporation and operational readiness are entirely different milestones. Banks must still comply with strict anti-money-laundering rules to verify beneficial owners. EU Inc creates a fast legal shell, but you will hit the exact same analog KYB wall before that entity can deploy capital.

Should we pause our upcoming European expansion until EU Inc is operational?

Absolutely not. The framework is stuck in the preparatory phase as of May 2026. Waiting for a perfect political framework bleeds market share. Execute your expansion using the national systems that exist today. Never stall regional revenue plans for an unproven regulatory promise.

Does the EU Inc structure harmonize local payroll and corporate tax obligations?

No. The Commission explicitly states this proposal is not intended to harmonise taxation or employee rights. Corporate tax and social security remain country-specific. You still need localized, rigid infrastructure to hire in Spain, run payroll in Poland, or manage compliance in France.

If the 48-hour registration is real, why do local providers quote 4-12 month setup timelines?

Because a legal filing is just step one. The 48-hour timeline only covers the business register interface. It completely ignores the actual heavy lift: UBO document collection, certified translations, notaries, apostilles, and tax registrations. The operational gap between a registered shell and a trading entity remains massive.

How will EU Inc impact our timeline for graduating from an Employer of Record (EOR)?

It will accelerate your exit. Right now, hard limits like Germany’s 18-month EOR cap force you to establish local entities. By reducing administrative burdens, EU Inc changes the math, making it faster and cheaper to own your permanent commercial footprint outright.