One of the most expensive mistakes in global expansion is treating “legally incorporated” and “operational” as the same milestone. I see that confusion in board updates, vendor proposals, and launch plans all the time. It creates the wrong timeline, the wrong budget, and the wrong internal expectations.

I have spent most of my career in regulated, jargon-heavy industries. The lesson has been consistent. Clear process beats vague reassurance. That applies directly to foreign subsidiaries.

At GEOS, we have mapped setup and management workflows in more than 80 countries. The biggest source of confusion is usually very simple: a company can be formed on paper and still be unable to hire, run payroll, invoice locally, or manage local compliance properly. For a hyper-growth company, that gap matters a lot.

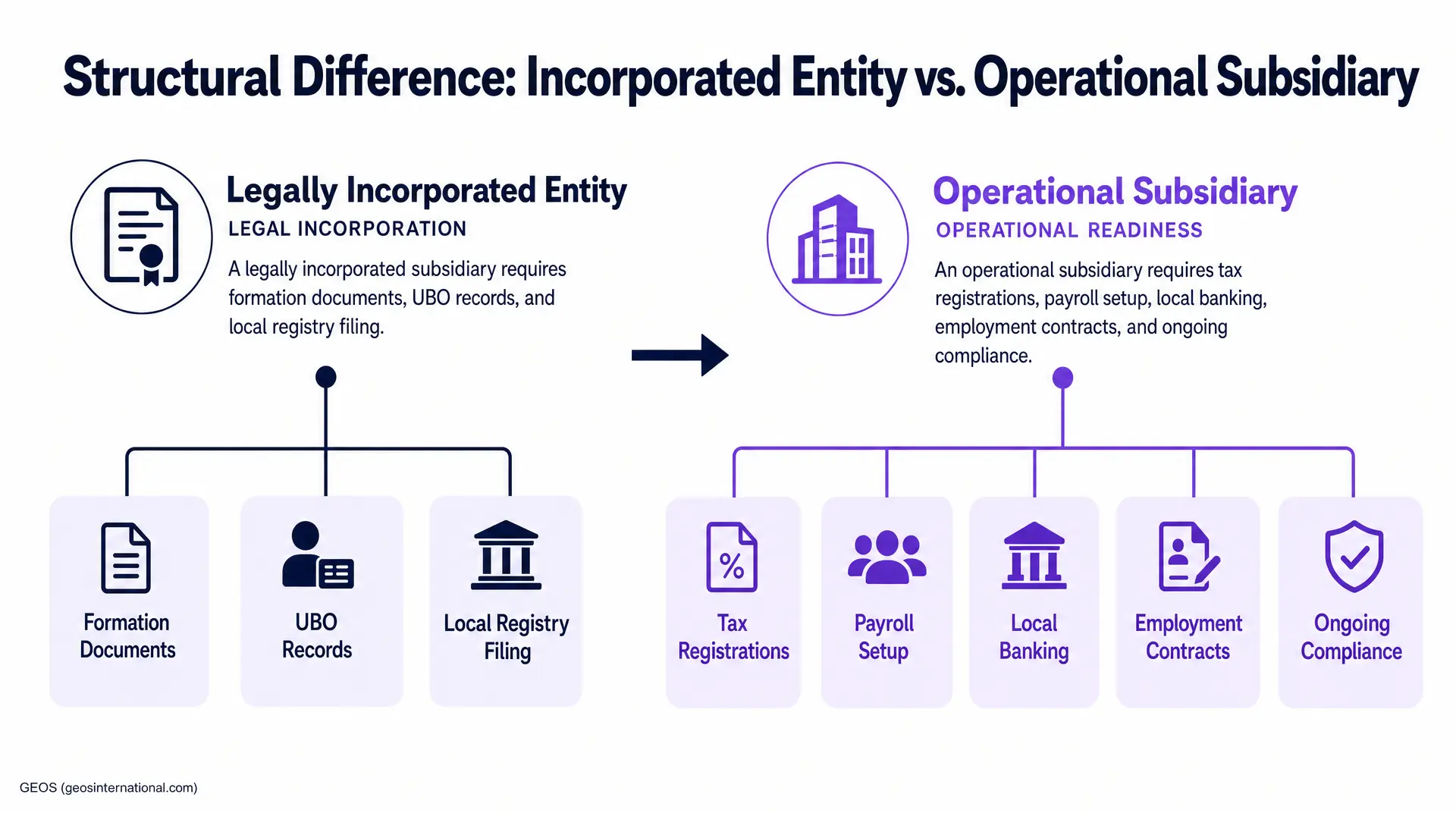

The Distinction That Changes the Whole Plan

A legally incorporated subsidiary is a company that has been formally created in the local jurisdiction. The incorporation has been filed, accepted, and registered. In many markets, that entity can remain dormant until it needs to become operational. The ongoing burden may be limited to basic annual or nil filings to keep it alive and in good standing.

An operational subsidiary is a different project. It has gone beyond the registry filing and completed the additional work required for its intended activity. That may include tax registrations, payroll setup, social security registrations, local banking, employment documentation, benefits administration, invoicing capability, treasury processes, and a governance model that keeps the lights on from a compliance perspective.

This distinction sounds obvious. In practice, it is where most expansion plans go off track. A company that wants future flexibility in a market is solving one problem. A company that wants to hire, sell, or transition employees off an Employer of Record is solving a much broader one. International expansion is an act of mutual problem solving. I always start with the same question: what exactly does this entity need to do?

What Legal Incorporation Actually Involves

Even the legal incorporation stage is more involved than most founders expect. The parent company usually needs to provide formation documents, ownership records, and identification for Ultimate Beneficial Owners and intended directors. Those documents often have to be certified, notarized, apostilled, translated, and couriered before the local filing can even begin.

That process changes by country. It can also change depending on the structure and home jurisdiction of the parent company. A US parent, a Canadian parent, and a UK parent may face different intake requirements in the same destination market. Local authorities may also come back with questions or require changes after the first submission. It is a meticulous process, and it has to be accurate.

A major source of delay often sits inside the parent company, not with the local registry. Busy CEOs and executives are not always available to review and wet-sign paperwork quickly. Some UBOs resist providing notarized identification or proof of address because of privacy concerns or because they are disconnected from the day-to-day business. When that happens, applications can stall or expire and restart.

This is one reason quoted timelines are wrongfully quoted almost every time. Many vendors describe only the narrow filing window. They do not include the intake work required before the filing, and they do not include the operating work required after it.

What Makes a Subsidiary Operational

Operational status depends on what the company is trying to do in the market. There is no universal checklist that applies equally to every country and every use case. The operating build has to match the business objective.

Employment Infrastructure

If the goal is hiring, complexity rises quickly. The subsidiary may need payroll and social security registrations, local employment contracts, benefits implementation, insurance coverage, and a local bank account. In some countries, a resident director or legal representative is mandatory. In others, pension or provident fund requirements are part of the basic operating stack.

This is where many companies discover that incorporation was only the first layer. A legally formed entity with no payroll setup and no local banking cannot actually employ people in a workable way. The business may have a certificate, but it does not still have an operating model.

This is also why EOR-to-entity transitions are often underestimated. In my experience, the hardest part is usually not the corporate filing. It is the legal continuity required when employees leave an EOR arrangement and sign new contracts with the local subsidiary. The communication has to be handled carefully. The sequencing has to be precise. If something goes wrong in an employee exit, local regulators may take a much closer look at the entire setup.

Revenue and Tax Infrastructure

If the goal is local revenue, a different set of requirements appears. The company may need corporate tax registrations, VAT or sales tax registrations, invoicing capability, AP and AR workflows, and a mechanism for transfer pricing and treasury between the parent and the subsidiary. If the company wants to contract directly with local enterprise or government buyers, those requirements become even more important.

Some companies do not need that full stack immediately. A business opening a light commercial presence may be able to validate the market first and delay the heavier operational build. Other companies need direct local contracting power from the start. That is why the same word, “setup,” causes so much confusion. The underlying project is different.

Governance and Ongoing Compliance

Operational status also means someone owns the post-incorporation work. Annual filings, director changes, address changes, resolutions, vendor coordination, and last mile tax filings still have to happen. That responsibility is often described as corporate secretarial support, but the title matters less than the function. Someone needs to make sure the entity stays in good standing.

I have seen how quickly that gets missed. GEOS remediated a Peruvian subsidiary that had fallen out of compliance because a departed shareholder was still listed as the legally required second shareholder. The entity had been formed, but the governance layer had broken. Restoring good standing required new documentation to appoint a replacement quickly.

Why Timelines Are Usually Wrong

Published timelines and vendor quotes often isolate the filing event and ignore the full sequence around it. The date may be technically defensible and commercially useless.

World Bank data show that business start-up timelines vary dramatically across countries, from roughly half a day in New Zealand to around 230 days in Venezuela. Even that benchmark uses the fastest possible procedure, which means it assumes ideal conditions and understates what foreign parent companies usually face in practice.

In my view, the common three-week quote is only realistic for baseline legal incorporation in a small number of markets, mainly the UK, US, and Canada. It almost never includes document collection, notarization, apostilles, translations, couriering, bank KYB, tax registrations, payroll registrations, or the work required to make the subsidiary truly operational.

For a fully operational subsidiary, 4 to 12 months is the more honest planning range in many jurisdictions. The exact timing depends on the country, the parent company’s structure, the business objective, and how quickly internal stakeholders provide required documents and signatures.

Country Examples That Expose the Gap

The difference between legal formation and operational readiness becomes clearer when it is viewed country by country. The variance is substantial.

Canada

Canada is one of the better examples of fast legal formation and slower operational reality. A foreign-owned Canadian entity can often be incorporated without the apostille-heavy document intake seen in many other countries. That creates the impression that the whole process is simple.

The structural choice still matters. Under Canada’s federal rules, 25% of directors must be Canadian residents, or at least one director if the board has fewer than four members. For foreign companies, that can turn a routine filing decision into a blocker. This is why I generally advise provincial incorporation, such as Ontario, rather than federal incorporation.

Operationally, Canada introduces a separate issue. The CRA environment is difficult for non-residents to navigate directly, so appointing an authorized Canadian representative becomes important early. If the business later expands into multiple provinces, extra-provincial registrations and annual filings add another layer of work.

Mexico

Mexico is a heavy lift from an operational perspective. Parent company documents often need to be notarized, apostilled, translated, and physically couriered. The local process is highly manual and highly dependent on proper sequencing.

Mexican tax law requires a local legal representative for a foreign-resident entity, and in practice that role is central for dealing with tax officials and wet-signing employment documents. That is one reason local representation cannot be treated as an afterthought.

If a foreign company tries to operate directly in Mexico rather than through the right local structure, the regulatory burden grows further. Mexican corporate law requires prior authorization before commercial registration and also imposes annual publication of an audited balance sheet for foreign-registered companies.

Payroll creates another bottleneck. Social security payments run through a narrow set of local banks, and only a small number are workable for foreign-owned entities. Ongoing payroll and accounting are also more nuanced than many foreign companies expect, with salaries often calculated more like a day rate than an annual salary. This is one reason I usually advise that companies need meaningful scale in Mexico before direct ownership delivers a strong ROI.

India

India often surprises founders because the incorporation itself can appear manageable. The operational layer is where the real project begins. A resident director is required. A traditional local bank account on the Indian rails is needed for TDS remittances and provident fund payments. Until those pieces are in place, the subsidiary may be legally formed and still unable to run payroll correctly.

This is also why many companies move from EOR to direct ownership in India at around 10 employees, particularly if they are building a global command center. The value of control becomes clearer at that stage, but the operating build still needs to be handled carefully.

Germany

Germany highlights the capital and banking side of the distinction. A standard GmbH requires €25,000 share capital, and the deposit certificate is an important gating item in the sequence. For startups, the UG can be a practical alternative because it can be formed with as little as €1 while profits are retained over time.

Even with the right entity type, Germany remains process-heavy. Parent company documents still need to be notarized, apostilled, and couriered into the country. Banking for 100% foreign-owned entities can also be a serious point of friction, which is why the right banking partner matters more than many founders expect.

The Service Model Matters as Much as the Country

The provider model can either clarify the process or turn it into a black box in terms of the steps that need to be taken. Founders often default to one of two extremes. They either hire the cheapest local lawyer they can find, or they hand everything to a Big Four firm and assume the premium price buys speed and certainty.

The low-cost local route can work for a single market. The problem appears once the company needs visibility, consistency, and coordination across multiple jurisdictions. Information is received piecemeal by email or phone calls. Every step is a surprise. The parent team ends up owning the project management while local advisors bill hourly and often incentivize dependency.

The Big Four route solves some of that and creates a different problem. I have seen it firsthand. The expertise is real, but the model is fragmented by region and often vague on scope. The client still has to re-share parent company context and documents with multiple country teams while paying for that glut of overhead.

Those patterns were part of the reason I co-founded GEOS. We later migrated a client with four global subsidiaries away from a Big Four provider by showing a clearer system of record and more transparent pricing. We also worked with a company that had more than 30 international entities and had lost visibility into compliance costs because local firms were invoicing subsidiaries directly. Untangling that required a dedicated full-time internal hire working alongside us. Without centralized visibility, managing a global footprint starts to feel like playing with a blindfold.

Technology Helps. Full Automation Does Not.

This space is still rooted in manual processes. By 2026, fully automated, human-free entity setup will still be a myth. Local officials continue to review applications manually. Wet-signed paperwork is still required in many places. Government portals are bespoke and generally not open to AI protocols.

Technology still plays an important role. It can map the workflow, centralize documents, assign owners, push notifications, and track compliance across multiple responsible parties. It can also show the compounding variance between legal incorporation and operational readiness in a way that email threads and PDFs never can.

That is the principle behind GEOS. We built software to expose the process, not to pretend the hard parts do not exist. The platform gives clients visibility into setup and ongoing compliance, while local experts still handle the on-the-ground tax, legal, and accounting work that cannot be abstracted away.

How I Advise Founders to Make the Call

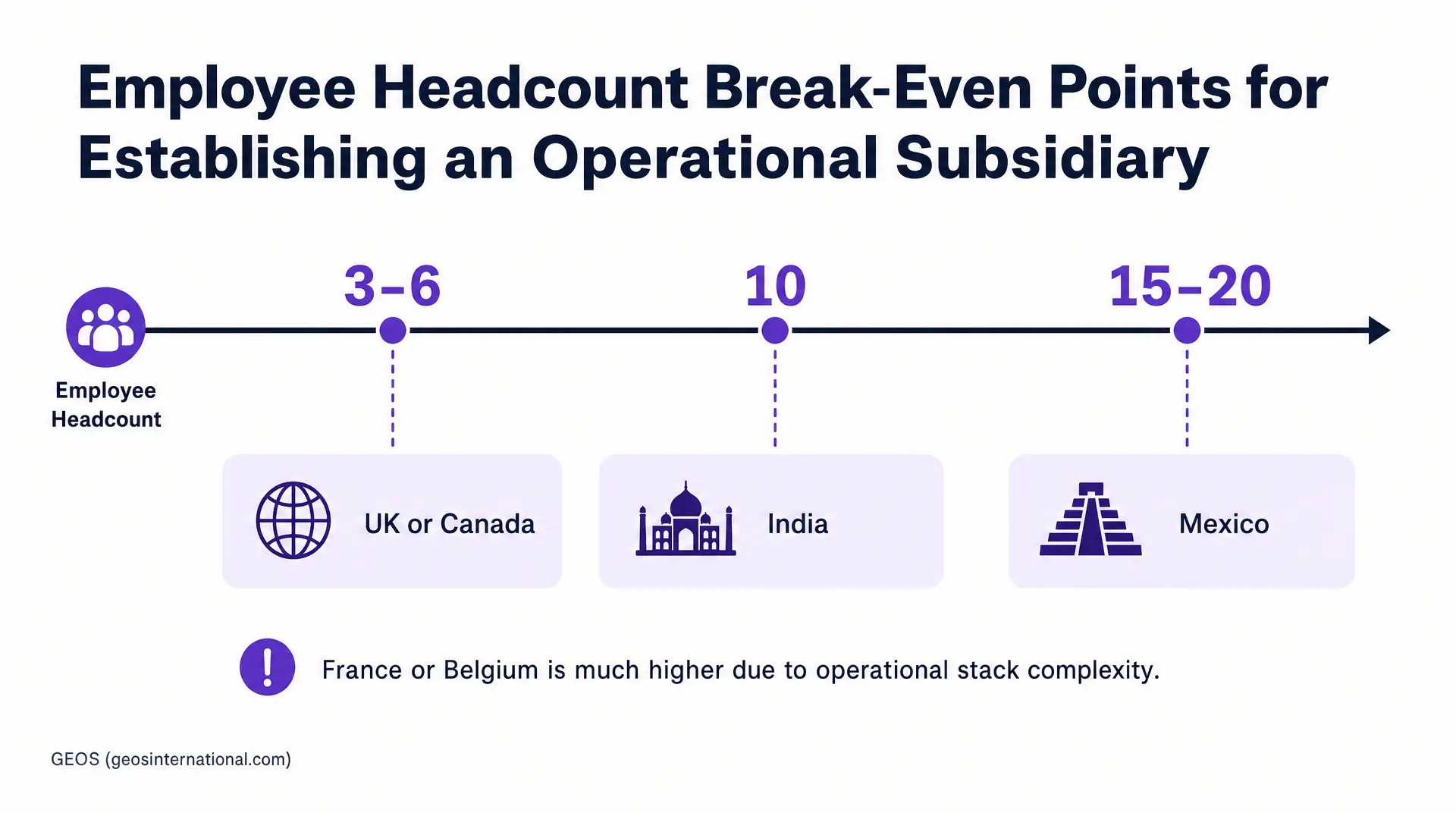

I usually advise founders to take a phased view. A global expansion journey has a beginning, middle and end. Early market validation can often be handled through contractors, an EOR, or a lighter local sales presence. Direct ownership becomes more compelling once the company has reached critical mass in a country or has multiple business reasons to justify it.

The break-even point varies widely. In the UK or Canada, I often see the math shift around three to six employees. In India, around 10 employees is common. In Mexico, 15 to 20 is a more realistic threshold. In France or Belgium, it can be much higher because the operational stack is more expensive and more complex. The headcount math also changes if the company needs local contracting power, tighter HR control, equity administration, or tax and revenue optimization.

Because GEOS is bootstrapped, I am biased toward sustainable execution and predictable ROI. That means defining activation criteria in plain terms before approving a launch. Does success mean the entity exists in the registry? Does it mean the bank account is open, payroll is live, tax registrations are complete, and the first invoice can be issued? Boards, finance teams, and operating teams should all use the same definition.

I also treat subsidiary formation as a permanent decision. Once a company enters a market through its own entity, someone has to own the ongoing operating model. If that structure is unclear on day one, the business will spend the next year trying to play catch up in terms of what was missed.

Final Word

The difference between legal incorporation and operational readiness is simple to describe and expensive to ignore. One creates a local legal entity. The other creates a business that can actually function in-market.

In 2026, the companies that move best internationally will be the ones that define the target state correctly, map the full process, and choose the right level of infrastructure for the real business objective. Fast filing still matters. Operational clarity matters more.

Frequently Asked Questions

How do we accurately forecast entity activation when reporting to the board?

Stop relying on best-case registry metrics. The World Bank ‘time to start a business’ metric explicitly uses the fastest possible procedure. It ignores banking and payroll setup. For a truly operational subsidiary, forecast 4 to 12 months to avoid missing board targets.

How do mandatory resident director laws impact our board’s control over foreign subsidiaries?

They create serious governance friction. Under Canada’s federal Corporations Act, at least 25% of directors must be Canadian residents. Appointing a third-party nominee fulfills this but dilutes immediate operational control. Structure at the provincial level instead to maintain total autonomy.

Should we optimize for minimum share capital to accelerate our initial European footprint?

Not if you want enterprise credibility. While you can legally form a German UG with just €1, a standard GmbH requires a minimum share capital of €25 000. Undercapitalizing delays your operational banking setup and signals instability to major clients.

Can a legally incorporated entity immediately sign commercial enterprise contracts?

Rarely. Legal incorporation does not equal commercial authorization. For example, Mexico’s General Companies Law mandates that foreign companies obtain prior authorization to operate commercially. Until you secure local tax IDs and regulatory clearance, your entity is entirely useless for revenue.

At what setup stage can we legally distribute localized equity to foreign leadership hires?

You cannot issue valid equity through a mere paper incorporation or an EOR. Your subsidiary must be fully operational, with active local payroll, tax infrastructure, and an established mechanism aligned with local securities law. Anything less risks severe regulatory blowback.