When I speak with CFOs about Ireland, I usually start with one distinction. Forming an Irish company is one milestone. Building an Irish entity that is operational, compliant, and manageable over time is a different project.

That distinction matters because this space is still rooted in manual processes. Timelines are often wrongfully quoted because the quote only covers the filing. It leaves out tax registrations and banking. It also leaves out payroll setup, registered office requirements, and the ongoing work required to keep the lights on from a compliance perspective.

My approach is practical and process oriented. At GEOS, we spent hundreds of hours mapping entity setup and management workflows across 80+ countries because there were no shortcuts. Ireland is one of the more attractive entry points into Europe, but even there, the quality of the setup depends on whether the full process is mapped from the start.

Key Takeaways

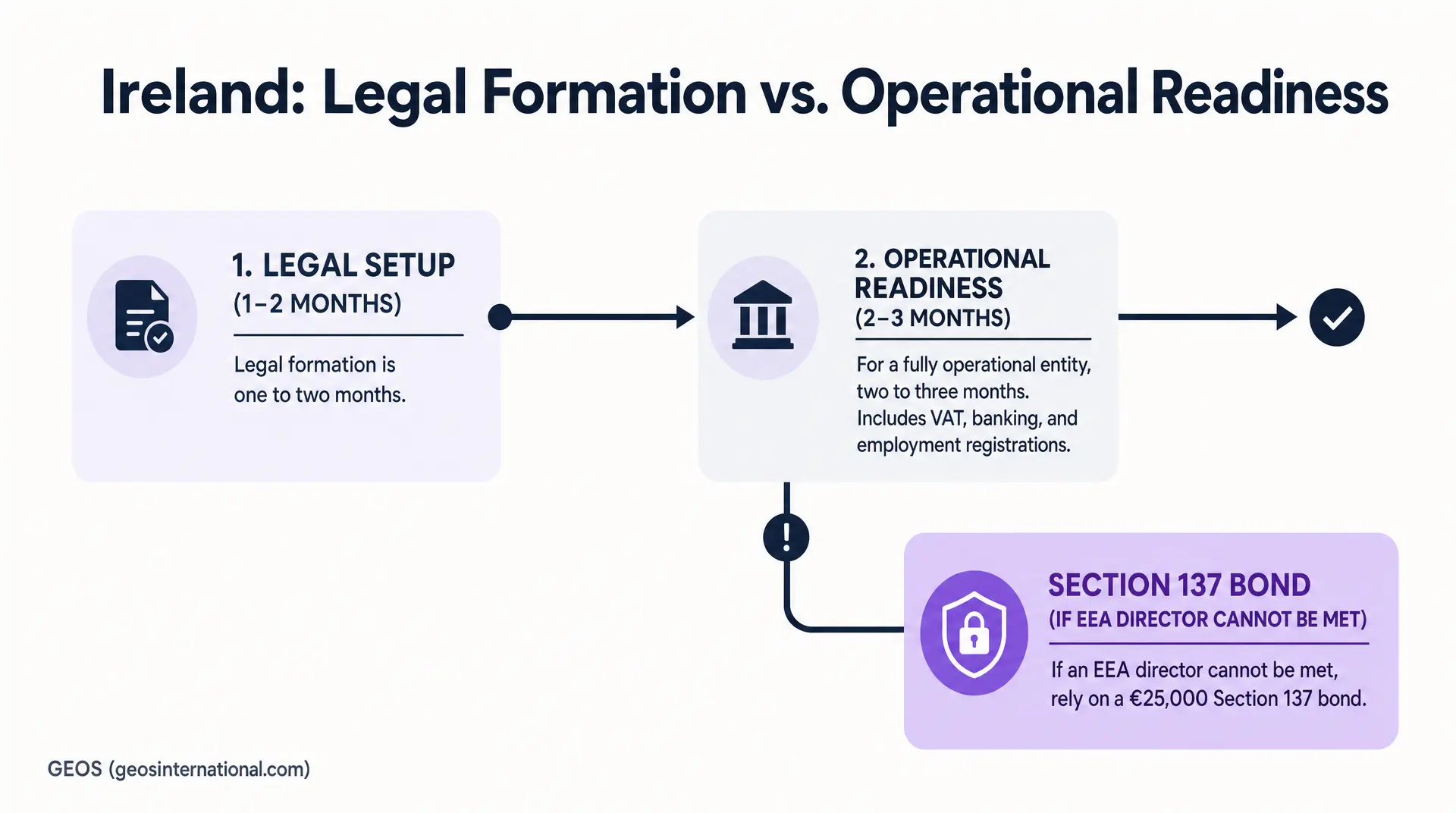

- While legal company formation in Ireland takes one to two months, achieving full operational readiness with VAT, corporate banking, and mandatory PAYE registrations requires a two to three-month timeline.

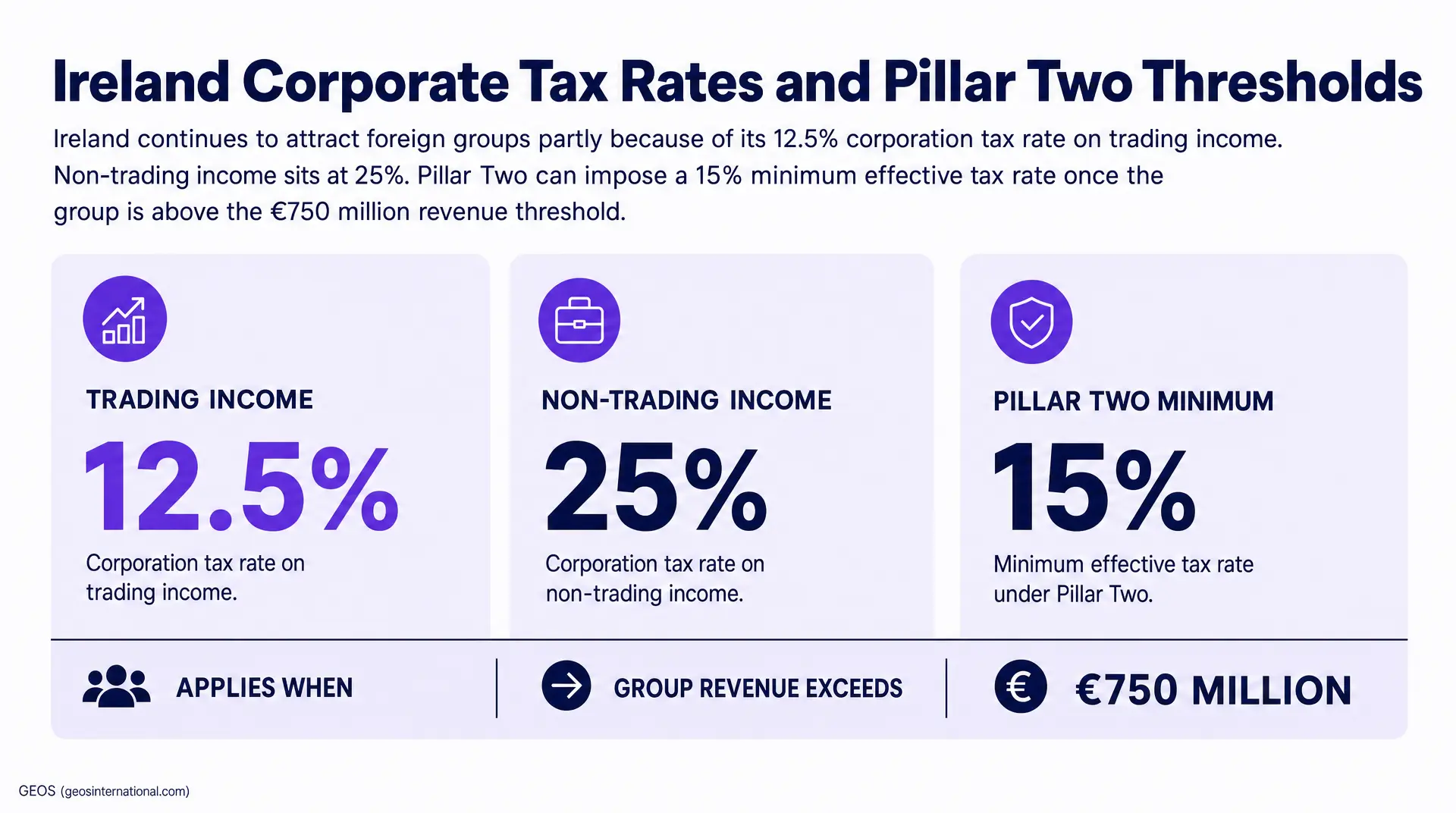

- Ireland applies a 12.5% corporation tax rate on trading income, but Pillar Two regulations impose a 15% minimum effective rate for enterprise groups exceeding €750 million in revenue.

- Foreign companies lacking an EEA-resident director for an Irish LTD can utilize a €25,000 Section 137 bond running for two years to avoid appointing an unrelated nominee director.

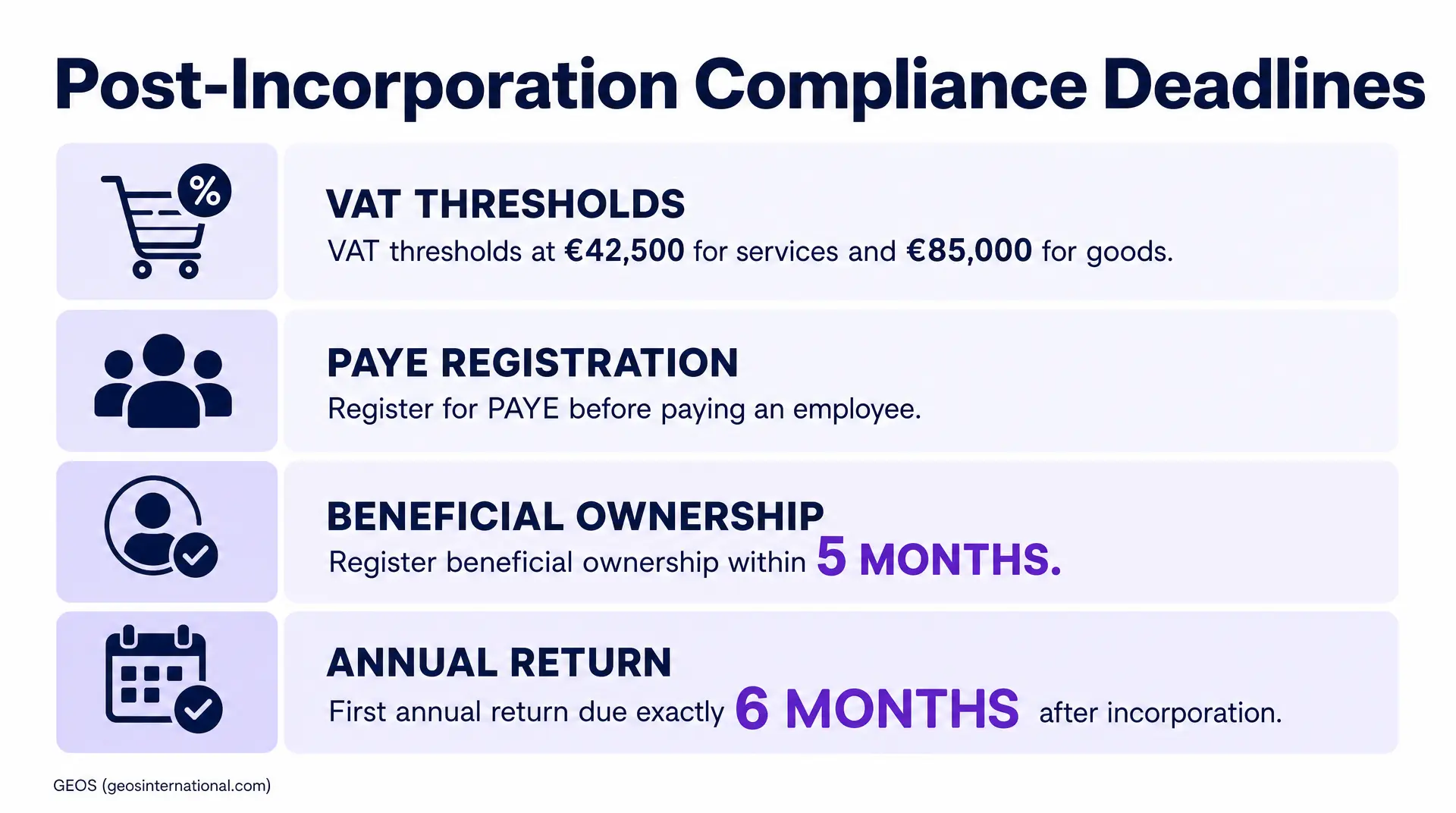

- Newly incorporated Irish entities must register ultimate beneficial ownership details within five months and file their first electronic annual return exactly six months after incorporation to avoid penalties.

- Foreign non-resident companies trading through a branch or agency in Ireland automatically fall within the Irish corporation tax charge because Revenue categorizes these structures as permanent establishments.

- Ireland recorded a 63% tertiary educational attainment rate among 25 to 34 year olds in 2023, significantly outpacing the 43% European Union average to support foreign direct investment.

Why Ireland Remains a Strong EU Entry Point

Ireland is one of the best jurisdictions for a foreign company that wants a credible foothold in the EU. It is English speaking. It has a strong reputation with foreign investors. It offers access to deep talent. It also has a long history of major technology companies using Ireland as their EU hub.

The tax profile remains part of that appeal. Ireland continues to attract foreign groups partly because of its 12.5% corporation tax rate on trading income. Non-trading income sits at 25%. Large in-scope groups need to read that with more nuance, because Pillar Two can impose a 15% minimum effective tax rate once the group is above the €750 million revenue threshold.

The operating environment also supports the case. IDA Ireland reported 323 investments in 2025, expected to create more than 15,300 jobs, while client-company employment reached 312,400. CSO data shows foreign-owned multinationals generated €920.6 billion in turnover and employed 623,128 people in the Irish business economy in 2022. In the Irish Information & Communication sector, 43.2% of employments were in US-owned enterprises in 2023.

The talent story is equally real. Ireland recorded a 63% tertiary attainment rate among 25 to 34 year olds in 2023, well above the EU-27 average of 43%. For finance leaders weighing an EU hub, those numbers reinforce what the market has already shown for years. Ireland is established, credible, and operationally attractive.

The tax profile helps. It is not the whole story. The right question is what the company needs Ireland to do.

The first platform dedicated to streamlining entity setup and management.

Start with the Objective, Not the Entity

I treat global expansion as an act of mutual problem solving. The first step is understanding the business objective with precision. Is Ireland being used to hire a small team, establish an EU hub, recognize local revenue, sign enterprise contracts, or create a tax-paying permanent establishment? Each path has a different timeline, cost structure, and risk profile.

That is why I do not like giving one universal Irish headcount threshold for leaving an EOR. In some countries, the break-even point is clearer and heavily driven by administrative difficulty. I often think about the UK or Canada very differently from France or Belgium because the operational burden is lower. Ireland sits closer to the more manageable side of that spectrum, but I still would not reduce the decision to headcount alone.

There are cases where incorporation does not need to happen immediately. If the company is only testing Ireland with one or two hires, an EOR can be completely appropriate. A company that only wants early commercial coverage may also decide to validate demand first and delay entity setup until there is a stronger operational reason to proceed.

I spent time on the EOR side before co-founding GEOS, so I am careful not to dismiss that model. It is often the best tool at the beginning of a global expansion journey. It is also materially safer than trying to classify a de facto employee as an independent contractor. Revenue’s code explicitly warns against false self-employment, and employers can be pursued for PRSI contributions over the full period plus penalties.

The analysis changes once Ireland is expected to do more than employ a small initial team. If the company wants to sign contracts locally, build an EU operating base, create a tax-paying presence, or gain more control over benefits, equity, and employment policy, direct incorporation usually deserves serious attention. Revenue also makes the permanent establishment issue very clear. A non-resident company trading through a branch or agency in Ireland is within the Irish corporation tax charge, and Revenue treats that concept as synonymous with a permanent establishment.

Formation in Ireland: Legal Setup Versus Operational Readiness

In Ireland, legal formation is relatively straightforward by European standards. In my experience, one to two months is a reasonable expectation to form the entity, especially if the residency solution is clear early. For a fully operational entity, I would plan on two to three months in total. That broader window is a better representation of reality because it includes VAT, banking, and any employment registrations that need to be completed before the company can actually function.

I spend time on this distinction because incorporation timelines in this market are often quoted too narrowly. The filing window gets presented as the full project. Finance teams then discover that the entity exists on paper but remains dormant until it needs to become operational. That gap is where frustration usually starts.

Official queue data also shows why “instant” is not the right frame. On May 27, 2026, the CRO said it was still processing ordinary A1 online submissions received on April 30. Ireland is more efficient than many jurisdictions, but it still operates inside real administrative queues.

Governance, Officers, and the Section 137 Bond

For most foreign scale-ups, the Irish vehicle is an LTD. That structure is flexible, but the officer rules still need to be planned properly. An Irish LTD can be set up with one director, but that requires a separate company secretary. Other Irish company types generally require at least two directors.

The residency rule is also more flexible than many founders first assume. Ireland requires at least one director who is resident in an EEA state, not necessarily in Ireland. If that cannot be met, the company can rely on a €25,000 Section 137 bond that must run for at least two years.

I generally advise foreign companies to use the bond route instead of appointing a nominee director where possible. It is cheaper. It is cleaner from a governance perspective. Most importantly, it avoids placing an unrelated individual on the board when that structure is not truly needed.

Tax, Payroll, and the Work That Makes the Entity Usable

Post-incorporation work is where many Irish projects start to drift. VAT is one example. Revenue’s VAT guidance sets thresholds at €42,500 for services and €85,000 for goods, but non-established persons can still have an obligation to register regardless of turnover in certain cases. VAT planning cannot be treated as a basic threshold exercise.

Corporate banking KYB sits in the same category. I include it in the operational timeline because it often lags behind the CRO filing. A company can be legally incorporated and still not be ready to run payroll, settle expenses, or support day-to-day operations.

Employment setup needs the same discipline. Irish employers must register for PAYE before paying an employee, and pay, tax, PRSI, USC, and other deductions must be reported on or before the payment date. PAYE also applies to directors’ income even if the company has no other employees. Those rules are simple to state. They still need to be built into the setup plan from the start.

Beneficial ownership is another step that can be missed when the project is received piecemeal by email. Newly incorporated Irish entities generally have five months from incorporation to register beneficial ownership details. In a subsidiary structure, that can mean tracing ownership through the parent until the relevant natural persons who hold or control 25% plus one share, or more than 25% ownership interest, are identified.

Client-side responsiveness also affects timing. One of the most common causes of delay in global entity setup is not the local authority. It is the parent company struggling to gather required documentation from Ultimate Beneficial Owners, or busy executives not having time to review and sign what is required. Ireland is more streamlined than many countries, but those internal bottlenecks still apply.

Entity Management in Ireland Is Where Budgets Usually Drift

Company formation is a project. Entity management is an operating model. When I refer to corporate secretarial work, I mean the filings and basic corporate actions required to keep the entity in good standing. It is the work that keeps the lights on from a compliance perspective. In Ireland, that sits alongside tax, accounting, payroll coordination, and registered office maintenance.

The annual return schedule catches many foreign companies off guard. Every Irish company, trading or not, must file an annual return electronically. The first annual return is due exactly six months after incorporation, and the filing must be completed within 56 days of the annual return date. Late filing can trigger penalties and can also affect audit exemption.

The registered office is another area where providers often gloss over cost and practicality. The CRO requires a physical location in the State for the registered office, and a standard PO Box is not acceptable. If the registered office changes, that must be filed on Form B2 within 14 days. For a foreign parent, that is a real operating requirement, not an administrative footnote.

This is why, when I evaluate an Irish provider, I ask for the full compliance calendar. I want accounting obligations, tax obligations, corporate secretarial deadlines, registered address requirements, and ownership by task. If a provider cannot show that in a coherent way, the client is entering a black box in terms of the steps that need to be taken.

The lowest-cost provider is rarely the lowest-cost outcome. Local accountants and lawyers can be effective for a narrow mandate, but they often work in a model that incentivizes dependency. Information is held locally. Billing is hourly. Every new issue becomes a separate instruction.

On the other end, the Big Four can offer safety and breadth. They can absolutely fit Fortune 100 or public companies. I have also been the client of PwC and seen how that model becomes fragmented by region. For a scale-up, the overhead often outweighs the benefit, especially when the client is still expected to coordinate multiple teams while paying a premium for the brand.

The problem gets larger once Ireland is one jurisdiction inside a wider footprint. Managing separate local advisors across several countries can become two or three full-time internal jobs just to process invoices, chase actions, and play catch up on what was missed.

The Operating Model I Trust

For cross-border entity management, I trust a centralized model. One account team should own the relationship under one logo and one umbrella. That team should coordinate with local legal, tax, and accounting experts behind the scenes. The client should not have to project manage multiple regional specialists directly.

Technology should be an enabler inside that model. I do not believe in fully automated entity setup. This work is still AI resistant for a while because local filings, government portals, and manual reviews remain stubbornly analog. What software can do very well is map the process, centralize documents, assign tasks, track deadlines, and make foreign compliance visible.

That visibility should be practical. If an Irish filing notice arrives, it should become a visible task and, where useful, a Slack notification. It should not sit in physical mail or an overlooked inbox. That is one of the biggest gaps I still see in this market.

This is how I approached building GEOS. We digitized the workflow and kept the human layer in place. We are supported by local experts, but the service delivery model stays centralized. We also keep the model vendor agnostic. In practice, that means a company can retain a strong Irish tax or payroll partner and still use GEOS as the system of record and oversight layer. I prefer that flexibility, and I also prefer predictable per-entity pricing because a company rarely needs the same service level in Ireland, Canada, and Mexico.

The value of that model shows up quickly. In one engagement, I demonstrated the GEOS platform and pricing model to a company managing four global subsidiaries. The business then canceled its incumbent vendor and transferred its compliance operations to GEOS because the platform gave them clearer oversight and more transparent pricing.

In another case, we supported a newly hired global compliance manager at a company with more than 30 entities. They had lost visibility into years of local invoices and unresolved obligations. Untangling the situation required years of backdating and work and auditing and untangling, alongside a dedicated internal hire. That example was not Ireland-specific, but the lesson applies directly. Foreign entity management fails when information is scattered, accountability is unclear, and each jurisdiction is allowed to turn into its own black box.

My View on Ireland

Ireland deserves its reputation. It is one of the strongest EU entry points for a foreign scale-up, especially one that wants a reputable English-speaking base, strong talent, and a workable operating environment. The tax profile helps. The deeper value comes from the combination of talent, credibility, and relative administrative simplicity.

The right setup still depends on why the company is entering. If Ireland is only being used to test a small hiring plan, an EOR can still be the efficient tool. If the company is building a genuine EU presence, wants local contracting ability, or needs a tax-paying establishment, the case for direct incorporation becomes much stronger.

In those situations, I would plan the full operating model upfront. I would use the Section 137 bond where it is the cleaner solution. I would build the compliance calendar before the company goes live. And I would not cheap out on provider selection simply because Ireland is more manageable than some other European jurisdictions.

That is the standard I use. A good Irish entity is formed on time, operational within a realistic timeline, and managed through a structure that gives finance real visibility from day one.

Frequently Asked Questions

When does an Irish subsidiary lose the 12.5% corporate tax rate?

The 12.5% trading rate holds for most, but CFOs must watch Pillar Two. If global revenue hits €750m+ recently, you face a 15% minimum effective tax rate. Model this into your OPEX.

Can we bypass EOR bloat by hiring Irish staff as independent contractors?

Revenue heavily polices false self-employment. Misclassifying workers creates massive exposure. You will owe backdated PRSI contributions for the full period plus severe penalties. If past the EOR break-even, just incorporate.

Are we required to register for Irish VAT immediately upon incorporation?

Mandatory VAT registration triggers when annual turnover exceeds €42,500 for services. However, non-established entities supplying taxable services locally may need to register irrespective of turnover. Centralize this oversight immediately.

What is the financial risk of missing an Irish corporate filing deadline?

Late filings destroy budgets. Missing your first annual return – due exactly six months after incorporation – strips away your audit exemption. For a scale-up, absorbing surprise statutory audit fees wipes out months of cost savings.

Do we need local payroll software if our Irish entity only has foreign directors?

Irish companies must register for PAYE before paying an employee. Crucially, PAYE applies to directors’ income even with zero local staff. Use a centralized compliance engine to manage these hidden obligations.