Most finance leaders know the tax and compliance rules of their home country well. The trouble begins the moment a company expands abroad. A subsidiary opens in France, Mexico, or India, and the finance team is suddenly working with almost no visibility. Invoices arrive. They get paid. Everyone hopes the work behind them was actually done.

I describe this to clients as playing basketball blindfolded. The player takes direction from teammates’ shouts because there is no way to see the court. That is how most companies manage their global subsidiaries today, and the model is finally breaking down.

What follows is how I think about subsidiary management heading into 2026. The old playbook is quietly expensive, and the alternatives have become far better than most CFOs realize.

The first platform dedicated to streamlining entity setup and management.

Key Takeaways

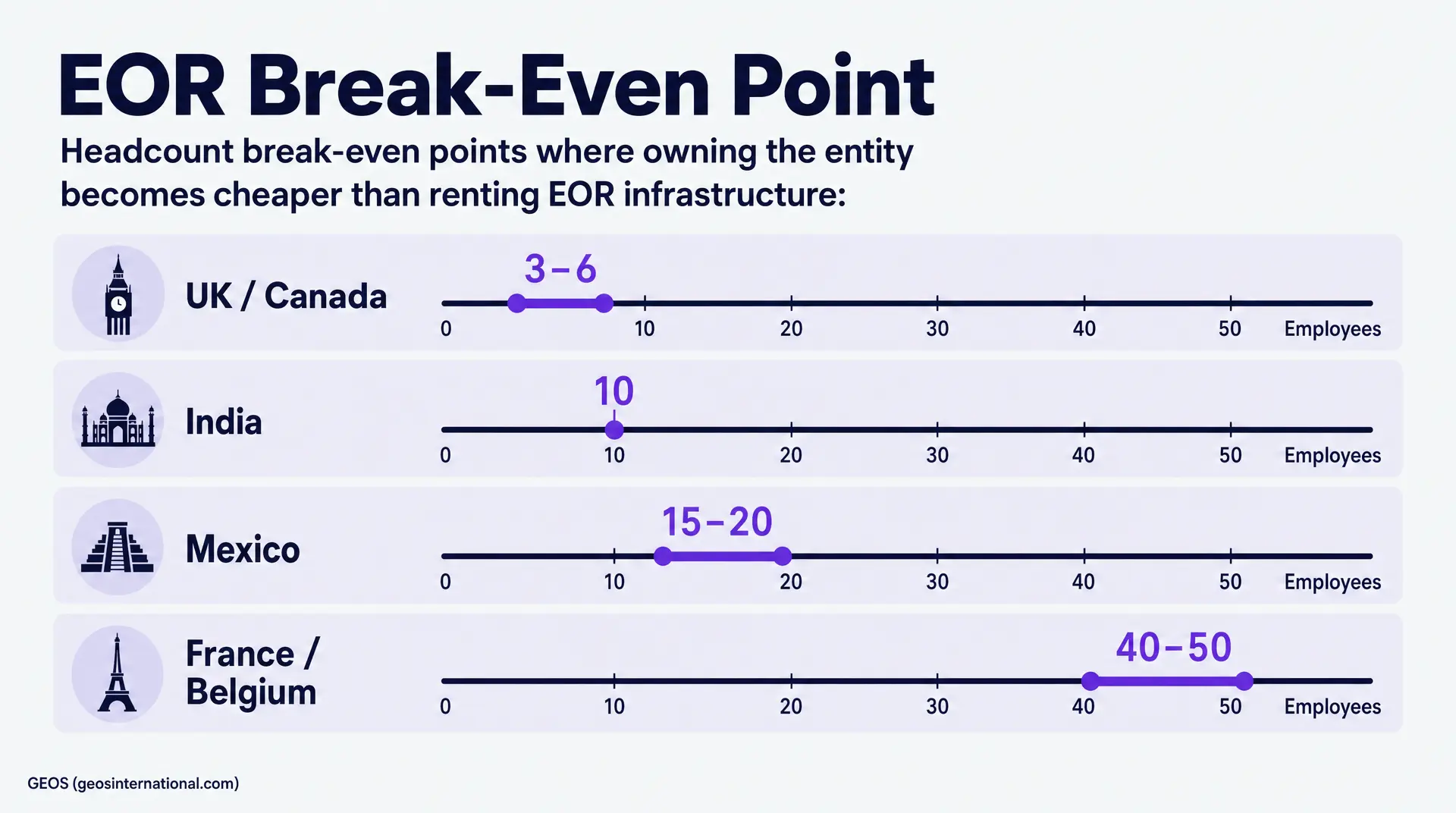

- Employer of Record models become more expensive than owning a local entity at 3 to 6 employees in the UK and Canada, 15 to 20 in Mexico, and 40 to 50 in France.

- Employer of Record contracts pass legal indemnity back to the parent company and cannot prevent permanent establishment tax risks when local regulators determine 5 to 20 employees constitute a taxable presence.

- Big 4 accounting firms routinely charge privately held scale-ups five to ten times more than necessary for global subsidiary setup by billing non-itemized fees without providing operational visibility into compliance tasks.

- Although artificial intelligence adoption among tax administrations reached 63.8% in 2022, OECD data confirms no surveyed authority uses AI for final administrative decisions, leaving global setup reliant on manual notarization.

- According to a 2026 TMF Group survey, 28% of global jurisdictions expect entity-management rules to grow more complex over the next five years, preventing near-term simplification of subsidiary compliance.

- The European Commission’s EU-Inc proposal for 48-hour digital corporate registration will not eliminate jurisdiction-specific analog hurdles like local payroll, social contributions, and value-added tax compliance.

- Centralizing global subsidiary management into a single system of record maps compliance workflows across 80 countries and establishes vendor-agnostic oversight at a predictable baseline cost

An Industry Still Operating in 1999

The global entity setup and management space has barely evolved since the 1990s. It runs on physical paper, black-box emails, and PDFs scattered across a dozen inboxes.

This is structural, not a matter of lazy people. It is genuinely difficult to deploy technology in a world built on analog local authorities, public notaries, and government agencies that still mail physical codes. So the industry stayed put.

That creates a specific problem: information asymmetry. A parent company rarely knows the “unknown unknowns” of operating in a new country. The local professional knows plenty, but has little incentive to share it coherently. The result is a small set of bad options, and each one leaves the finance leader blind. None of this is fading, either. TMF Group’s 2026 survey found that 28% of jurisdictions expect entity-management rules to grow more complex over the next five years, with another 51% expecting no change. Planning around this reality matters far more than waiting for it to simplify.

Where the “Insurance Policy” Breaks Down

The first option is the legacy route: a Big 4 firm or a global conglomerate like PwC, Deloitte, TMF, or Vistra. Most CFOs justify the six-figure price as insurance against compliance failure.

I have been a client of PwC. I am not speculating about where that insurance breaks down once the subsidiary goes live.

The pitch is real on paper. These firms have tax experts, legal experts, compliance experts, and regional experts. The problem is that those teams are split by geography. Setting up entities in three countries means working with three separate teams. Each engagement restarts from scratch, and the parent company context has to be re-explained every time. The client ends up acting as the project manager of their own expansion.

Then the invoice arrives. These firms charge a premium, and the work is often summarized in one or two vague line items, something like “corporate compliance associated with the subsidiary.” There is no breakdown of what was actually done. When there is no visibility into the work itself, the risk of overpaying purely for insurance becomes very real.

Big 4 firms suit a Fortune 100 or a publicly traded enterprise well. A privately held scale-up is a different story. Most of those clients are subsidizing bloated operations that cost five to ten times more than they should.

The Black Box at the Other Extreme

The second option swings the other way: hire a cheap single-market accountant or lawyer in each country. On paper, it is the lowest-cost path. Over a multi-year horizon, it is often the most dangerous.

The experience is a true black box. Every step arrives as a surprise, whether that is unexpected documents, unexpected fees, or unexpected delays. Many local providers actively withhold the full compliance picture from foreign clients. Their model bills by the hour, so withholding information is not an accident. It is a way of incentivizing dependency.

Now multiply that across several countries. Managing a web of independent local vendors generates so much administrative overhead that it can consume two or three full-time internal roles. The work amounts to chasing invoices and trying to figure out what actually needs to happen.

I have seen where this leads. One company came to us with more than 30 global entities and no visibility into their compliance costs, because local firms were invoicing each subsidiary directly. Untangling years of backdated work and unverified invoices was so complex it required a dedicated full-time hire working alongside our team. That is the true cost of the “cheap” route.

The EOR Math: When a Smart Tool Becomes a Liability

Most scale-ups are running a third strategy today: the Employer of Record. I spent time on that side of the table at Borderless AI, so let me be precise about it.

Criticism of EOR often goes too far. It is genuinely one of the best tools available for early global hiring. A company adding its first few employees in France or Belgium should use one without hesitation. It is cheaper, faster, and far easier to manage than a local entity.

Every global expansion journey has a beginning, a middle, and an end. EOR is built for the beginning. The problem is that thousands of companies are now over-leveraged on it, paying long after the math stopped working. The scale is published in the open. Remote lists EOR pricing at $599 per employee per month on an annual rate. Ten employees on that model run close to $6,000 a month in platform fees alone, before salary, benefits, or local taxes.

There is a break-even point in every country where owning the entity becomes cheaper than renting infrastructure. That point varies sharply. In the UK and Canada, it sits around three to six employees, because both are easy, low-cost jurisdictions. In India, it is closer to ten, often because companies scale quickly to run a global command center. Mexico lands around 15 to 20, given its heavier ongoing tax and accounting load. France and Belgium can reach 40 to 50, because setup and maintenance there are genuinely hard.

That variance is not arbitrary. TMF Group’s 2026 complexity index ranks Mexico as the second most complex jurisdiction in the world and France fourth, while Canada sits at 58th and the UK at 69th out of 81. The economics track directly with that complexity. The base incorporation step reflects it too. Companies House registers a UK company within 24 hours for £100, while Canada’s federal route runs CAD $200 online on a one-business-day standard.

So a company sitting on 10 UK employees through an EOR is losing money. Set the monthly per-employee fee against the cost of a UK entity plus ongoing compliance, payroll, and tax, and the decision becomes straightforward.

Headcount is not the only trigger. The moment a company needs to recognize local revenue, sign a commercial lease, win enterprise or government contracts, offer equity, or build a bespoke benefits package, an entity belongs on the table immediately. An EOR cannot provide the legal standing for any of that.

The Liability Argument You Will Hear

An EOR representative will often make one last case to keep the account: “Stay with us and we absorb the legal liability and the tax audits.”

That argument does not survive a close read of the contract. EOR agreements are structured around shared liability. When something goes wrong because of the parent company’s actions, and the parent company is the one directing the employee’s daily work, the contract passes liability and indemnity straight back to the client.

The published terms confirm it. Remote’s service terms state that the client must supply accurate data on paid time off, hours worked, and overtime, and that employment fees can include fines, penalties, and legal fees except where the fault is solely the provider’s. The provider also states it will not be liable if a government body later determines the employee actually belongs to the client.

There is a second exposure an EOR cannot remove: permanent establishment risk. Somewhere between five and twenty employees in a single country, depending on local stance, regulators may decide the company has created a taxable presence. The Canada Revenue Agency, for example, treats a corporation as having a permanent establishment where an employee or agent has general authority to contract on its behalf. The company has taken on the risk without ever gaining the control.

One more caution, because the mistake is common. A company should never run an EOR in a country where it already operates a tax-paying entity. Local authorities view that split setup as a worse posture than having no entity at all.

What the 2026 Approach Actually Looks Like

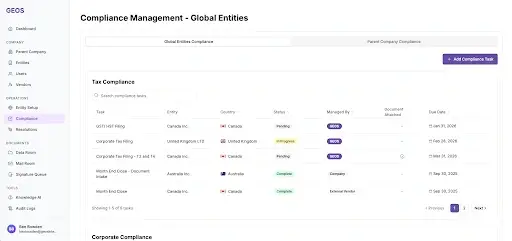

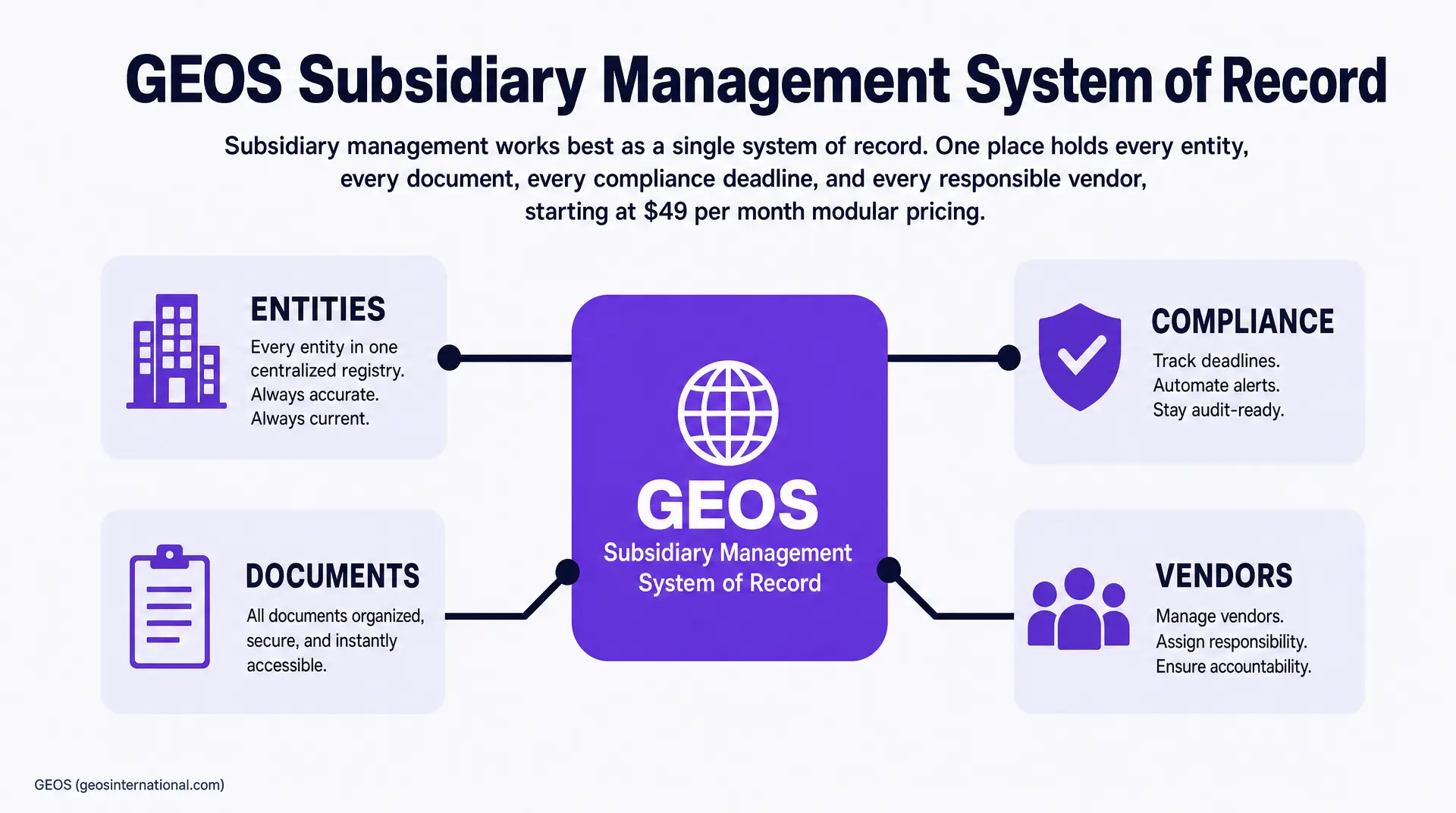

If the established options leave a finance team blind, bloated, or both, the alternative starts with a shift in framing. Subsidiary management works best as a single system of record. One place holds every entity, every document, every compliance deadline, and every responsible vendor.

This is the core of what we built at GEOS. We spent hundreds of hours mapping exactly what it takes to set up and maintain an entity in more than 80 countries. Every step, every filing, every variance. The compliance tasks that keep an entity in good standing change not only by country, but by the specific business activity inside that country.

The shift becomes obvious the first time a foreign tax notice from Mexico is scanned, logged, and pushed directly to a Slack channel rather than disappearing into physical mail. For an executive who only ever knew their home country’s compliance, that is the moment the whole court comes into view.

Three things make this model work for a risk-focused CFO. The first is predictable, modular pricing. Our platform starts at $49 per month per entity. A company with 10 subsidiaries chooses the tier for each one based on what that country actually requires. There is no hourly inflation, and the cost can be forecast to the dollar.

The second is a vendor-agnostic oversight layer. Boards tend to question this piece: if clients bring their own local vendors, how is quality guaranteed? The platform exists precisely to provide that scrutiny. We bring preset mappings of what compliance should look like in a given country, then measure a client’s existing vendor against that standard. Workflows prompt accountants for completion and require receipts when tasks are done. A company can keep a cheap single-market accountant or a Big 4 firm and finally gain real visibility into both.

The third is that technology does not replace people here. We maintain regional teams and a pre-vetted network of local lawyers, CPAs, and resident directors who handle the on-the-ground work. The platform is the organizing layer that keeps anything from slipping through the cracks. It centralizes communication rather than removing it.

The combined effect places GEOS in the middle of the market: far more transparent and efficient than the local black box, at roughly a fifth of what the Big 4 charge.

The Case Against Waiting for AI

Every finance leader eventually asks whether it makes sense to wait for AI to deliver one-click incorporation. My answer is no, and the reason is a distinction that matters.

There is a wide gap between a citizen incorporating in their own country and a foreigner setting up a subsidiary. The first is close to one-click, because the infrastructure is built for residents. The second is not.

A foreign company still has documents that must be certified, notarized, apostilled, couriered, and translated. Public notary appointments still happen in person. Banks still run stringent checks on foreign-owned entities. Government agents still review applications by hand. Even a heavily digitized market proves the point: France’s Guichet unique processed 4.2 million business formalities in 2024, still still routes those filings for validation through INSEE, commercial-court registries, tax services, and social-security bodies.

The data on tax authorities reinforces this. OECD research found that AI use among tax administrations rose from 29.8% in 2018 to 63.8% in 2022, still a 2024 inventory found no surveyed tax administration using AI to make final administrative decisions. The technology supports the work. It does not own it.

AI belongs in this picture as an enabler. Our assistant, Geovanna, can instantly answer which provinces a client is registered in across Canada, drawing on that client’s own global footprint. It does not carry out filings or make legal decisions. Automation here is about project management and visibility. Anyone promising a fully automated entity setup is selling a false promise.

The Case Against Waiting for EU-Inc

The same logic applies to the EU-Inc framework, which has generated real excitement among finance leaders. On March 18, 2026, the European Commission presented a formal proposal for an EU Inc. corporate framework, targeting fully digital registration within 48 hours at a maximum cost of €100.

This is genuinely positive news, and it should encourage more companies to expand into Europe. It is also not operational law. The Commission has asked Parliament and Council to reach agreement by the end of 2026, which leaves the real timeline uncertain.

More importantly, a unified framework will not erase the country-specific realities underneath it. VAT registration, local payroll, social contributions, and cross-border tax will still need handling jurisdiction by jurisdiction. Those analog hurdles are not going anywhere soon.

Pausing European expansion to wait carries a steep opportunity cost. The wait will be long, and the market share handed to faster competitors will not come back. Building now, with the tools that already exist, is the better decision.

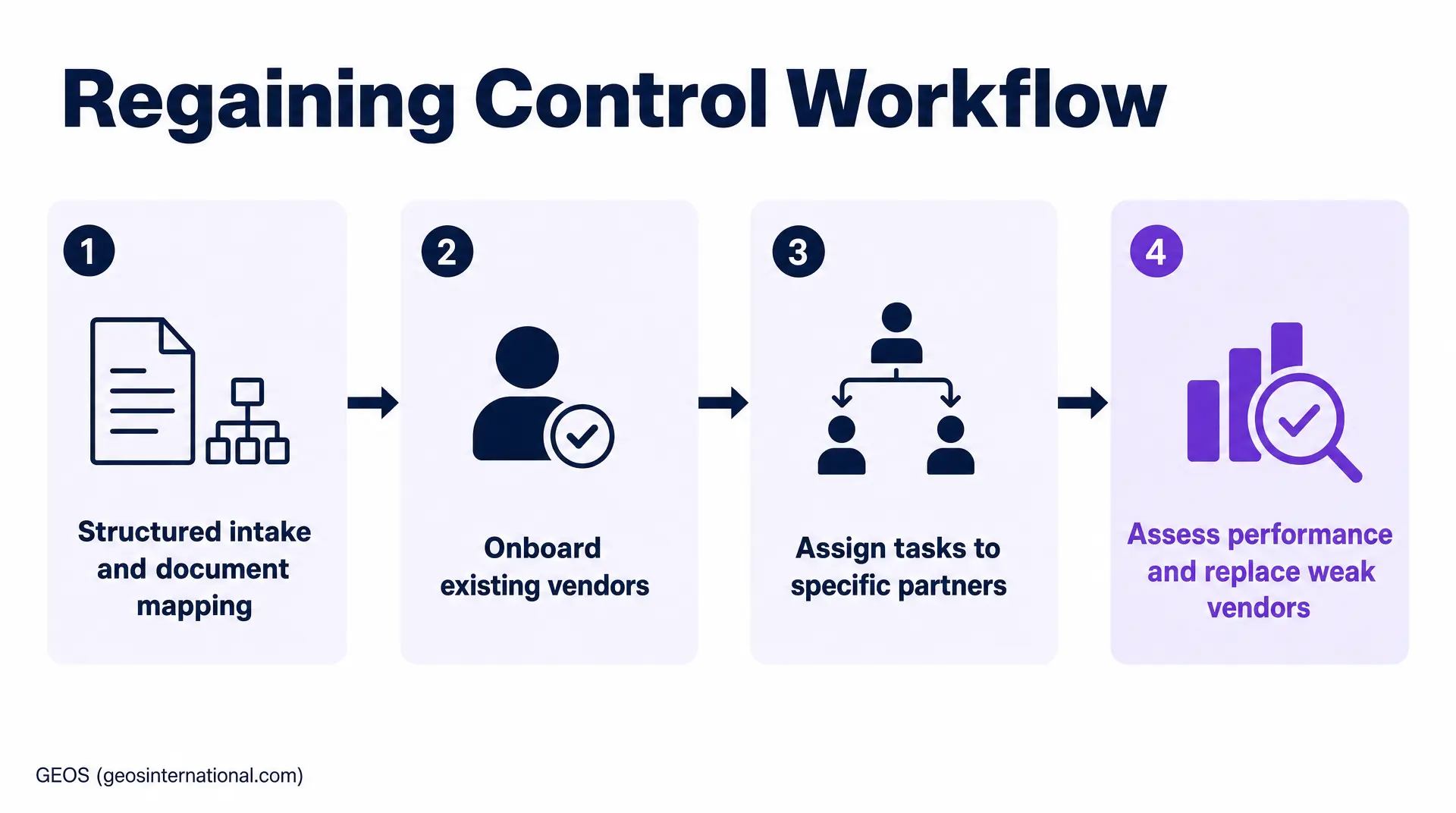

Regaining Control

Taking action looks concrete. When a client arrives buried in subsidiaries, the first step is a structured intake. We organize every document on file, build a dedicated page for each entity, and pre-map the global compliance tasks already due in that country.

From there we onboard the client’s existing vendors and assign each task to the right party: tax to the tax partner, payroll to the payroll partner. We track down the final 5 to 10% of tasks specific to that client, such as a VAT threshold registration. Then we assess whether the current vendors are actually performing. The strong ones stay. The weak ones get replaced.

This shift from blind to in control can happen fast. We showed one company managing four global subsidiaries our platform and our transparent per-entity pricing. They canceled their legacy Big 4 vendor and moved everything to us, because for the first time they could see exactly what they were paying for.

The companies that win the next phase of global expansion will not be the ones who paid the most for insurance, waited for AI, or held their breath for EU-Inc. They will be the ones who demanded visibility now. Subsidiary management was a black box for three decades. It does not have to stay one.

Frequently Asked Questions

Does a subsidiary automatically shield the parent company from Permanent Establishment (PE) risk?

No. A separate legal entity doesn’t erase operational realities. The Canada Revenue Agency warns that if an employee retains general authority to execute contracts for the parent, you still risk triggering a taxable presence. True risk mitigation requires strict operational separation, not just incorporation.

How do we audit legacy foreign vendors when acquiring a company with existing subsidiaries?

Stop relying on their self-reporting. You must establish a vendor-agnostic oversight layer. Map the exact statutory requirements for each jurisdiction, then measure inherited vendors against that baseline. If they resist submitting work proofs through a centralized platform, replace them. Opacity is a choice. Don’t finance it.

Why do foreign bank account setups stall even after we incorporate successfully?

Corporate registries and financial regulators operate in different centuries. Despite fast entity registration, post-incorporation hurdles remain analogue. In Mexico, TMF Group notes banking demands physical presence and wet-ink signatures. Never forecast your operational launch based solely on the incorporation timeline.

What are the hidden liabilities when moving a large team off an EOR into our own subsidiary?

The exposure hides in the transition data. Terminating contracts requires meticulous classification. According to Remote’s guidance, mishandled terminations or inaccurate leave records trigger immediate payroll fines, litigation, and co-employment risk. Audit all accrued liabilities before transferring staff to your entity.

Should we rely on our local counsel to forecast changes in subsidiary compliance regulations?

Relying solely on local counsel guarantees blind spots. Their model monetizes hourly reactions, not proactive strategy. According to TMF Group’s 2026 survey, 28% of jurisdictions expect entity-management penalties to become more complex within five years. You need a centralized system of record, not a reactive lawyer.