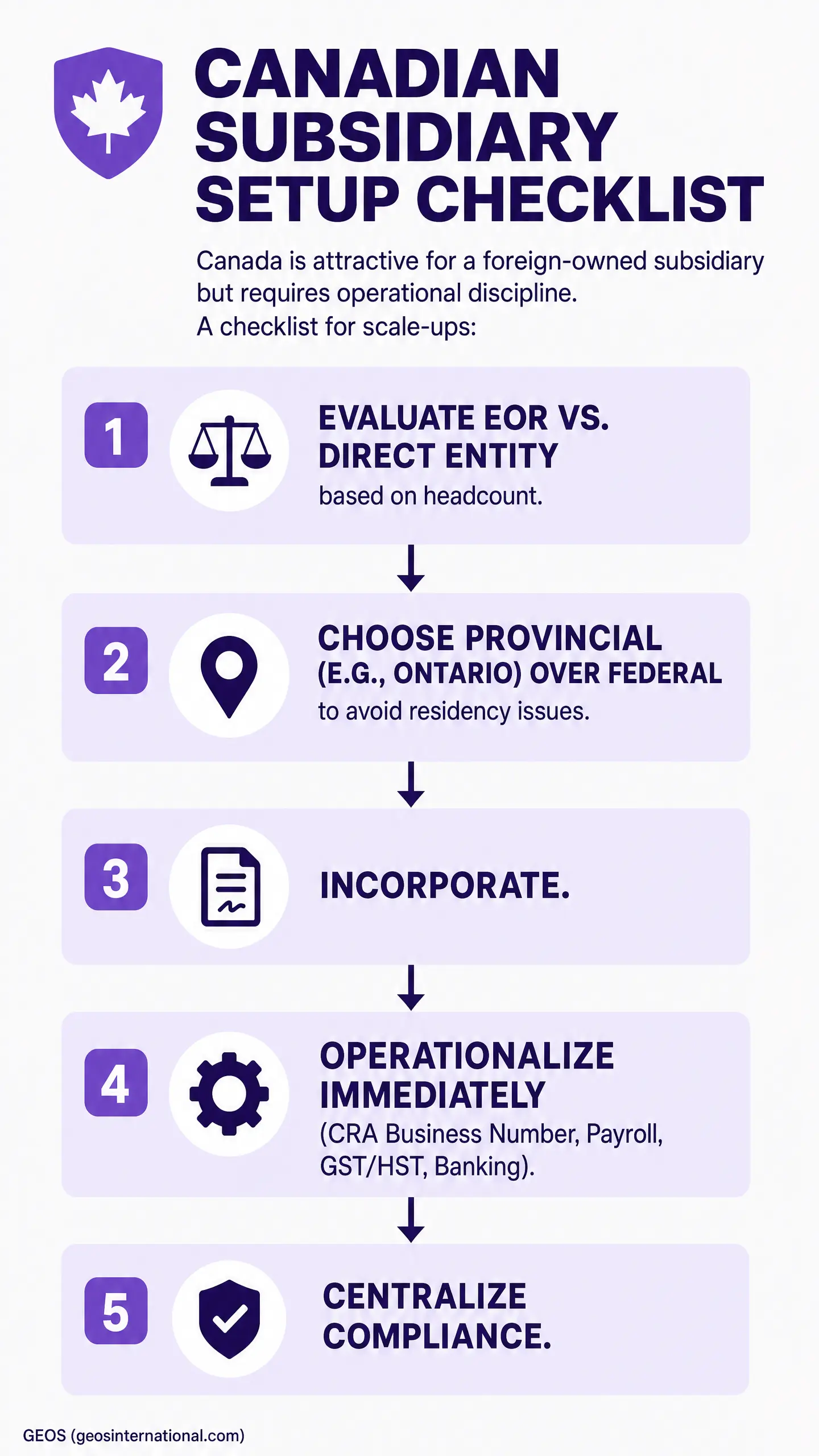

Canada is one of the more attractive markets for a foreign-owned subsidiary. The setup burden is lighter than what most companies face in Europe, Latin America, or parts of Asia. That is exactly why founders often underestimate it.

In my experience, Canada creates a specific kind of false confidence. The filing can move quickly, so the whole project gets framed as a quick legal task. Then the company realizes the real work sits after incorporation. Tax visibility, payroll, banking, and inter-provincial compliance are what determine whether the entity can actually operate.

At GEOS, we have mapped entity setup and management across more than 80 countries. Canada is still one of the simpler jurisdictions. A historical benchmark makes the point clearly. The World Bank’s final Doing Business profile ranked Canada 3rd for starting a business, ahead of France at 37th and Japan at 106th. The directional point still holds. Canada is comparatively easy. It still needs to be operationalized properly.

This guide is how I would structure the checklist for a scale-up opening a wholly owned Canadian subsidiary. It is written for operators who care about speed, but also care about getting the first payroll, first contract, and first quarter of compliance right.

Key Takeaways

- The World Bank’s 2020 Doing Business profile ranked Canada third globally for starting a business, making subsidiary setup significantly faster than in markets like France or Japan.

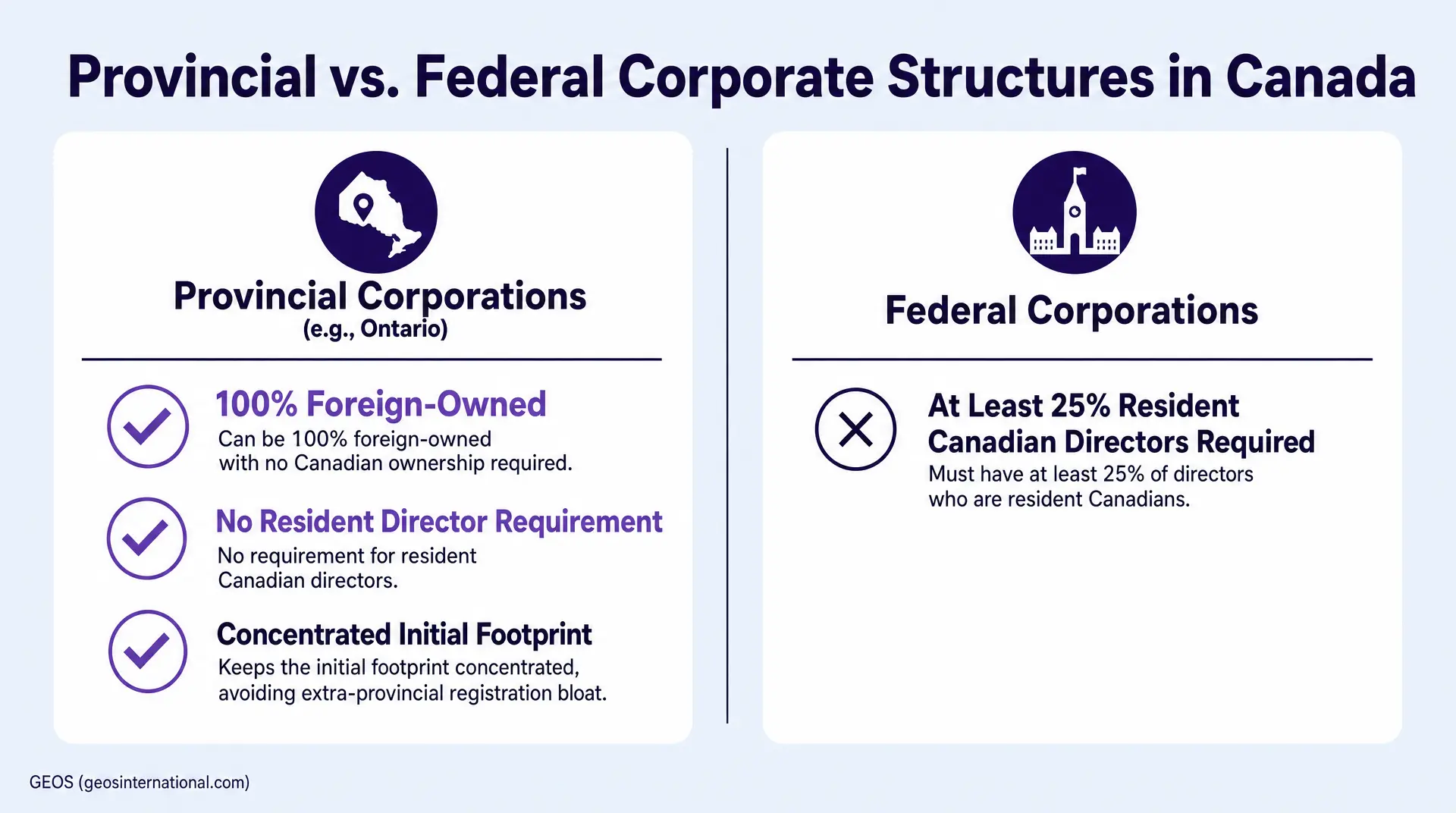

- Foreign-owned subsidiaries should choose provincial incorporation over federal incorporation to avoid the Canada Business Corporations Act requirement that at least 25% of directors be Canadian residents.

- Foreign founders frequently lose tax visibility into Canadian subsidiaries because the Canada Revenue Agency restricts online business account access to individuals possessing a valid Social Insurance Number.

- Setting up a traditional Canadian bank account triggers strict FINTRAC verification, requiring extensive beneficial ownership documentation for any foreign individual controlling 25% or more of corporate shares.

- Canadian subsidiaries must register a Goods and Services Tax account as soon as local taxable supplies exceed a $30,000 threshold over the relevant reporting period.

- Expanding a subsidiary into Quebec introduces a separate compliance layer, requiring companies to manage distinct provincial income tax and pension contributions directly through Revenu Quebec.

1. Start with the Business Case, Not the Filing Fee

We do not start with incorporation documents. It’s important to start with the reason the entity needs to exist.

That sounds basic, but it matters. A global expansion journey has a beginning, middle, and end. If the company only needs one or two early hires, an Employer of Record can still be the better tool. If the market is only being tested, there may be lighter ways to enter Canada before committing to a full entity. Speed is important, but so is using the right instrument for the stage of growth.

I am also very cautious about companies trying to shortcut Canadian hiring through contractor structures that are really employment in disguise. Under federally regulated employment standards, a paid worker is presumed to be an employee unless proven otherwise. That is why I generally view EOR as the safer early-stage compliance tool when headcount is low.

Canada changes the math sooner than many founders expect. It is one of the easiest and cheapest countries to set up compared with France, Japan, or Brazil. In practical terms, that means the break-even point between EOR and a direct entity can arrive earlier. I have said elsewhere that in straightforward markets like Canada, the move can start to make sense at a relatively low headcount, often well before companies would consider it in France or Belgium. If the company also wants direct control over benefits, equity grants, local contracts, or enterprise credibility, the case becomes even stronger.

Once a company has reached critical mass in Canada, continuing to rent infrastructure through an EOR often stops being efficient. The monthly fee is one part of the equation. Control is the other. Companies eventually want their own compliant employment vehicle, their own payroll decisions, and their own commercial presence.

2. Choose the Legal Structure Before Optimizing for Speed

Provincial Incorporation Is Usually the Practical Answer

For most foreign-owned subsidiaries, my recommendation is to start with a provincial corporation, usually in Ontario, rather than defaulting to federal incorporation.

Founders often assume federal is the premium version. On paper, it can look appealing. Corporations Canada lists online federal incorporation at 1 business day with a $200 filing fee. Ontario lists immediate online processing with a $300 government fee. That filing difference is marginal. It should not drive the decision.

The real issue is director residency. Under the Canada Business Corporations Act, a federal corporation must usually have at least 25% resident Canadian directors, and if there are fewer than four directors, at least one director must be a resident Canadian. Many foreign parents cannot satisfy that requirement cleanly. In that situation, I do not see value in appointing a nominee director in Canada simply to chase a federal structure.

The national naming argument is also weaker than many people assume. Corporations Canada says a federally approved word name gives the corporation the right to use that name across Canada, but it also says approval does not guarantee protection against other corporate names, business names, or trademarks. For a foreign-owned scale-up, that benefit is often overstated. If the structure cannot satisfy the residency requirement, the strategic upside is limited.

A provincial corporation is usually cleaner from a governance perspective. It can be 100% foreign-owned. It avoids adding unnecessary board complexity. It also aligns with how most scale-ups actually enter Canada, which is by concentrating initial activity in one province.

The first platform dedicated to streamlining entity setup and management.

Keep the First Footprint Concentrated

Canada is a single country from a market standpoint. It is not a single compliance environment.

My preference is to keep the first footprint tight. If the team is starting in Ontario, build the entity around Ontario. If the first hires are in Toronto, do not over-engineer for a national footprint on day one. Canada rewards focus.

The reason is inter-provincial complexity. A company may need to register in each province or territory where it conducts business. In practice, that concept can extend beyond major revenue. It can include an address, a phone number, or offering products or services in the jurisdiction. Ontario’s own extra-provincial regime shows how quickly the burden starts to add up. Ontario lists an extra-provincial licence at $330 with 5 business days of online processing.

Quebec deserves separate treatment in any Canadian checklist. I consistently flag Quebec as the most complicated province for inter-provincial expansion because it introduces another revenue authority and another operating layer. A company that expands there too casually can create a complicated web of items very quickly.

3. Build the Setup Package Before Filing

Canada removes one of the biggest friction points that shows up in other countries. For a foreign-owned Canadian subsidiary, the setup generally does not require the parent company documents to be notarized, apostilled, and couriered around the world. That is a meaningful advantage.

It still makes sense to prepare the file with discipline. The company should have its parent-company details, ownership structure, director information, registered office details, and signer availability aligned before the filing starts. In my experience, global setup delays are often caused by executives being too busy to review and sign straightforward documents. Canada is easier than Germany or Mexico, but signer delays can still cause a wrench in things.

This is also the stage where expectations should be set properly. Legal formation may move in days or weeks. Operational readiness takes longer if tax and banking are not being handled in parallel. That distinction matters. A dormant entity on paper is not useful to a growth-stage company trying to hire, invoice, or sign commercial commitments.

4. Incorporate the Subsidiary, but Treat Filing as the Midpoint

Once the structure is chosen and the inputs are ready, the incorporation itself is relatively efficient.

This is where Canada can feel deceptively simple. The legal filing is one of the fastest parts of the project. A company can receive incorporation documents quickly and still be nowhere near operational. I see this issue often. Founders celebrate the filing and then realize there is no CRA visibility, no payroll account, and no bank account capable of supporting the intended use case.

My approach is process-oriented. I map the legal step and the operational steps together from the beginning. That avoids the black box in terms of the steps that need to be taken. It also avoids the common situation where every step is a surprise and the client has to play catch up in terms of what was missed.

5. Make the Entity Operational Immediately After Incorporation

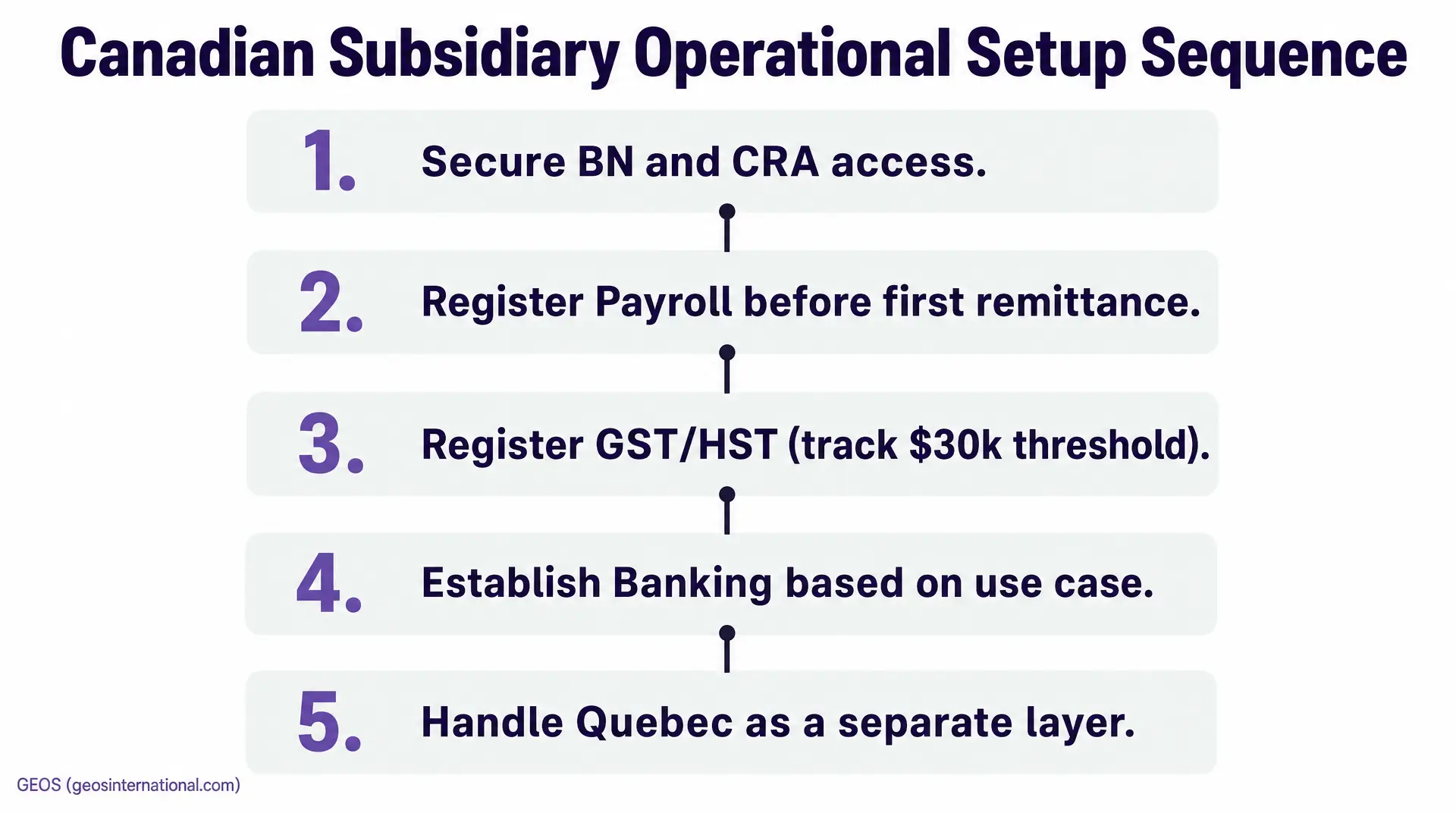

Secure the Business Number and the Right CRA Access

The Canadian tax layer starts with the Business Number. The CRA describes it as a unique 9-digit identifier. Payroll, GST/HST, and other tax program accounts sit under that core number rather than existing as unrelated identifiers.

For foreign-led subsidiaries, the practical issue is not just registration. It is ongoing access. The CRA says business information online can only be accessed when the relevant individual has the right profile, including a name and SIN on file where applicable. That is why foreign founders often discover that the entity exists, but no one on the parent side can efficiently see or manage what is happening.

The practical fix is to appoint a trusted representative early and scope the authority properly. The CRA allows different levels and scopes of authorization, including access limited to payroll or GST/HST rather than the full account. In most cases, that is the cleanest way to create operational tax visibility quickly.

This has become even more important because the CRA no longer accepts BN or program account registration by phone. Non-residents must now use the online non-resident business registration process. That change reduces one form of friction, but it does not eliminate the access issue. A representative model is still the most efficient way to keep the lights on from a compliance perspective.

Register Payroll Before the First Payroll Run Is Due

This is one of the most common misses in a fast launch.

A Canadian employer needs a payroll program account if it is paying salaries, wages, bonuses, benefits, or allowances. If the entity does not already have the payroll account, it must be registered before the first remittance due date. That sounds obvious. It still gets missed because many teams focus on the legal formation and assume payroll can be layered on later without consequence.

For a scale-up graduating from an EOR or making its first direct Canadian hires, payroll setup should be treated as part of the launch sequence, not as an administrative follow-up. If the company intends to run payroll in week one, the registration work has to be completed before week one.

Register GST/HST When the Operating Model Requires It

GST/HST is the next area where timing matters. Registration becomes mandatory once taxable supplies exceed $30,000 over the relevant threshold period. Companies can also choose to register earlier where that makes operational sense.

The key point is that GST/HST should be considered early if the Canadian entity will invoice locally, recover input tax, or support a broader commercial model. This is not something to leave until the finance team discovers a threshold was crossed retroactively.

Choose the Right Banking Path Based on Use Case

Canadian banking is one of the few areas where foreign founders still run into meaningful friction.

The decision should be based on what the Canadian entity will actually do. For simple payroll runs and straightforward local expenses, a fintech option can often be sufficient. It is usually faster to set up remotely and is more accommodating to foreign ownership. For higher transaction volume, more complex treasury needs, or substantial local revenue, a traditional Canadian bank may still be necessary.

The reason bank setup can slow down is structural. FINTRAC guidance requires reporting entities to verify the company’s existence and beneficial ownership. That includes records showing the company’s name, address, directors, and beneficial owners, including individuals who own or control 25% or more of the corporation’s shares. For a foreign-owned group, that can turn into a heavy KYB exercise very quickly. If a traditional bank is required, in-person travel may still be part of the answer.

Treat Quebec as a Separate Operating Layer

Once a company hires or pays employees through a Quebec establishment, the payroll and tax picture changes materially.

Revenu Quebec requires employers to handle Quebec source deductions and employer contributions, including Quebec income tax, QPP, QPIP, and other employer-side items. For a company with a single Ontario team, that is irrelevant. For a company scaling nationally, it is one of the clearest examples of why Canadian expansion should be staged carefully.

6. if the Company Is Graduating from an EOR, Plan the Transfer as a Legal Project

Canada is one of the countries where EOR can stop making sense earlier because the entity setup itself is relatively efficient. Once the headcount grows, the company often wants a better ROI, cleaner governance, and more control over local employment.

The difficult part is not the incorporation. The difficult part is the legal continuity of moving employees from one arrangement to another. In every country, including Canada, that means handling notice periods, contract transitions, benefits continuity, and employee communication carefully. A rushed handoff can create avoidable friction with the team and with local compliance.

I also generally advise against keeping an EOR arrangement running indefinitely in a jurisdiction where the company already has its own active entity. Local authorities tend to view that as a worse posture than using an EOR before the entity exists at all. Once the company has committed to a direct Canadian subsidiary, the operating model should be consolidated around it.

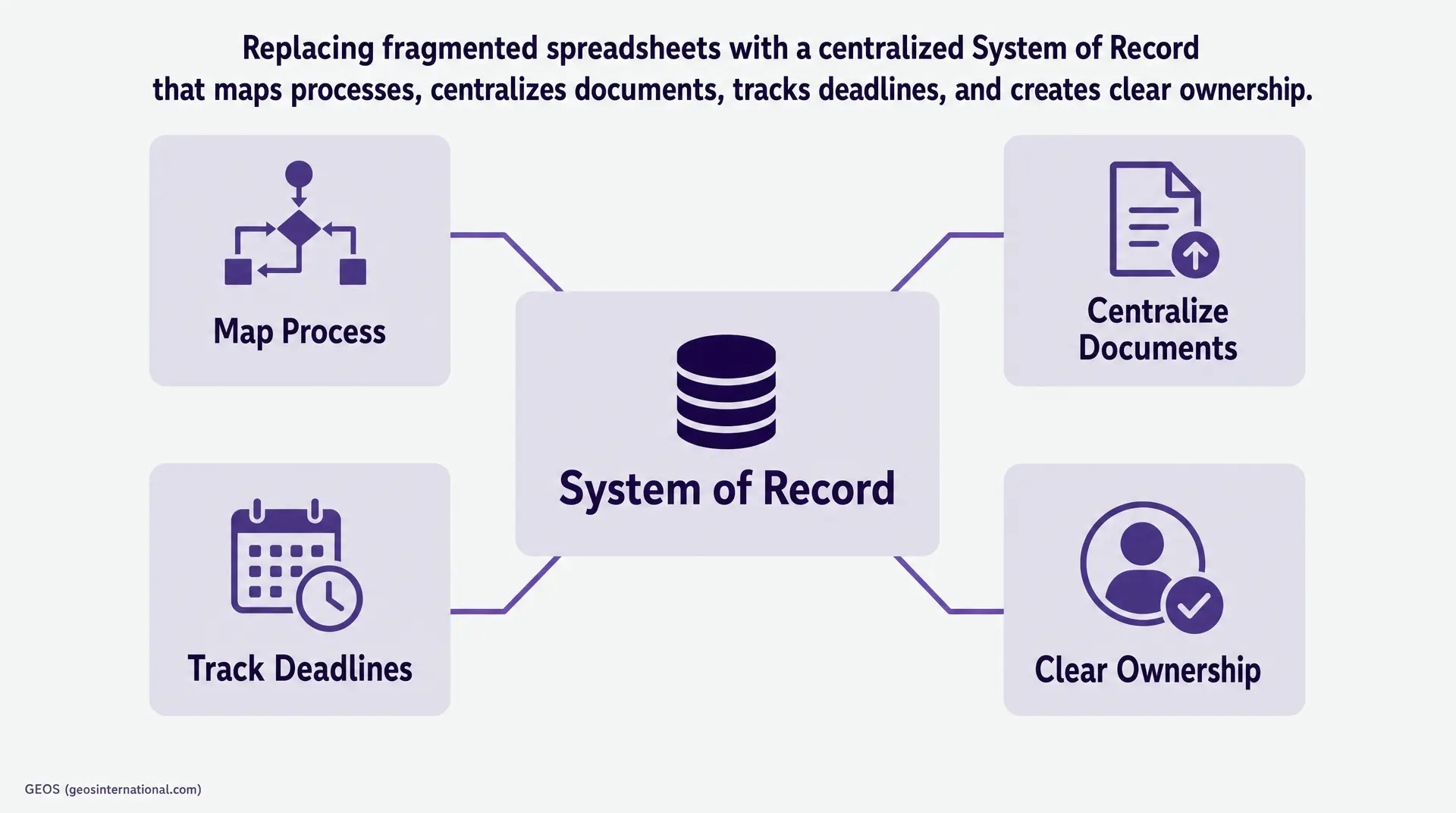

7. Put Compliance Into a System of Record

Opening the subsidiary is only half the job. The rest is entity management.

This is where many companies start playing with a blindfold. Information gets received piecemeal by email or phone calls. Local vendors handle isolated tasks. The parent company loses visibility into what has been filed, what is due, and what is still outstanding. That dynamic gets worse once the footprint moves beyond one entity.

I have seen the consequences directly. In one engagement, I demonstrated the GEOS platform and pricing model to a company managing four global subsidiaries, and the business moved away from its existing Big Four provider. In another, we supported a newly hired compliance manager at a company with more than 30 entities and had to work through years of backdating, auditing, and unverified local vendor invoices. Those cases were global, not Canada-specific, but the lesson applies directly to Canada as well. A fast initial setup means very little if the company later loses control of deadlines, tax correspondence, and local service accountability.

My view is straightforward. Technology should be an enabler. It should map the process, centralize documents, show deadlines, and create a clear ownership model. It should not replace the human layer. Canada is simpler than many markets, but it still operates through real agencies, real filings, and real local nuance.

8. the Practical Checklist, in Order

For a foreign-owned scale-up, the Canadian checklist runs in a clear sequence. First, confirm that a direct entity is actually justified now and that the company has reached the point where direct ownership offers better control or ROI than an EOR. Next, choose the structure with a bias toward provincial incorporation, usually Ontario, and avoid creating unnecessary governance issues through a federal model that requires resident directors. Then prepare the corporate inputs properly so the filing is not delayed by missing ownership details or unavailable signers.

After incorporation, move immediately into operational setup. Secure the Business Number and the right CRA access model. Register payroll before the first remittance deadline. Assess whether GST/HST registration is already required or should be done proactively. Choose the banking path based on the entity’s actual operating model, not on brand familiarity. If expansion beyond one province is planned, stage those registrations deliberately and treat Quebec as a separate layer of planning. Finally, put the entity into a real compliance operating system so ongoing corporate and tax tasks are visible and controlled.

Canada is a favorable jurisdiction. That is precisely why it should be approached with discipline. The country removes many of the physical hurdles that slow foreign incorporation elsewhere. The remaining work is concentrated in tax administration, payroll readiness, banking, and provincial complexity. If those pieces are handled in the right order, a Canadian subsidiary can move quickly and operate cleanly from the start.

Frequently Asked Questions

Do we need to lock up paid-in minimum capital to incorporate in Canada?

No. Unlike many European jurisdictions, the World Bank notes Canada requires 0% paid-in minimum capital. This allows you to deploy capital directly toward hiring and local GTM efforts rather than parking cash in a dormant corporate bank account just to satisfy antiquated legal prerequisites.

How strictly does Canada enforce contractor misclassification if we delay entity setup?

Very strictly. Under federal standards, a paid worker is explicitly presumed to be an employee unless proven otherwise. Bypassing an entity by disguising employees as contractors invites immediate compliance orders. Use an EOR for initial testing, then graduate to a wholly owned subsidiary.

Ontario incorporation is immediate, but what is the actual time-to-activation?

While Ontario legally incorporates you immediately for a $300 fee, operational readiness takes weeks. Activating payroll accounts, combined with heavy FINTRAC KYC requirements for any beneficial owner holding 25% or more equity, dictates the actual timeline for processing your first local payroll.

Can an Ontario provincial subsidiary directly sign enterprise deals in other provinces?

Not automatically. A provincial corporation must register wherever it ‘conducts business,’ which includes offering services locally. Operating across borders adds a compliance burden. For example, an extra-provincial licence typically requires additional government fees and 5 to 10 days of processing time. Plan inter-provincial expansion deliberately.

How do foreign founders manage CRA tax accounts without a Canadian SIN?

Since November 2025, non-resident businesses must register online, but direct portal access still requires a SIN. The practical fix is delegating a trusted professional as an authorized representative with Level 2 or Level 3 access to manage your BN, payroll, and GST/HST accounts seamlessly.