Speed matters in global expansion. I have always preferred a B-plus plan executed today over an A-plus plan next week. Foreign subsidiary setup, however, is one of the few areas where speed without visibility usually creates more delay later.

I learned that from both sides of the market. Before co-founding GEOS, I worked in highly regulated B2B environments and later spent time within the EOR model up close. I was also part of the company’s internal effort to set up entities globally with a Big Four firm. That experience made one point very clear: the visible legal quote is rarely the real cost.

At GEOS, we later spent hundreds of hours mapping entity setup and ongoing entity management across 80+ countries. There were no shortcuts. This market is still rooted in manual processes, local protocols, and very wide country-by-country variance. The hidden cost for founders is often not knowing what they do not know in every jurisdiction.

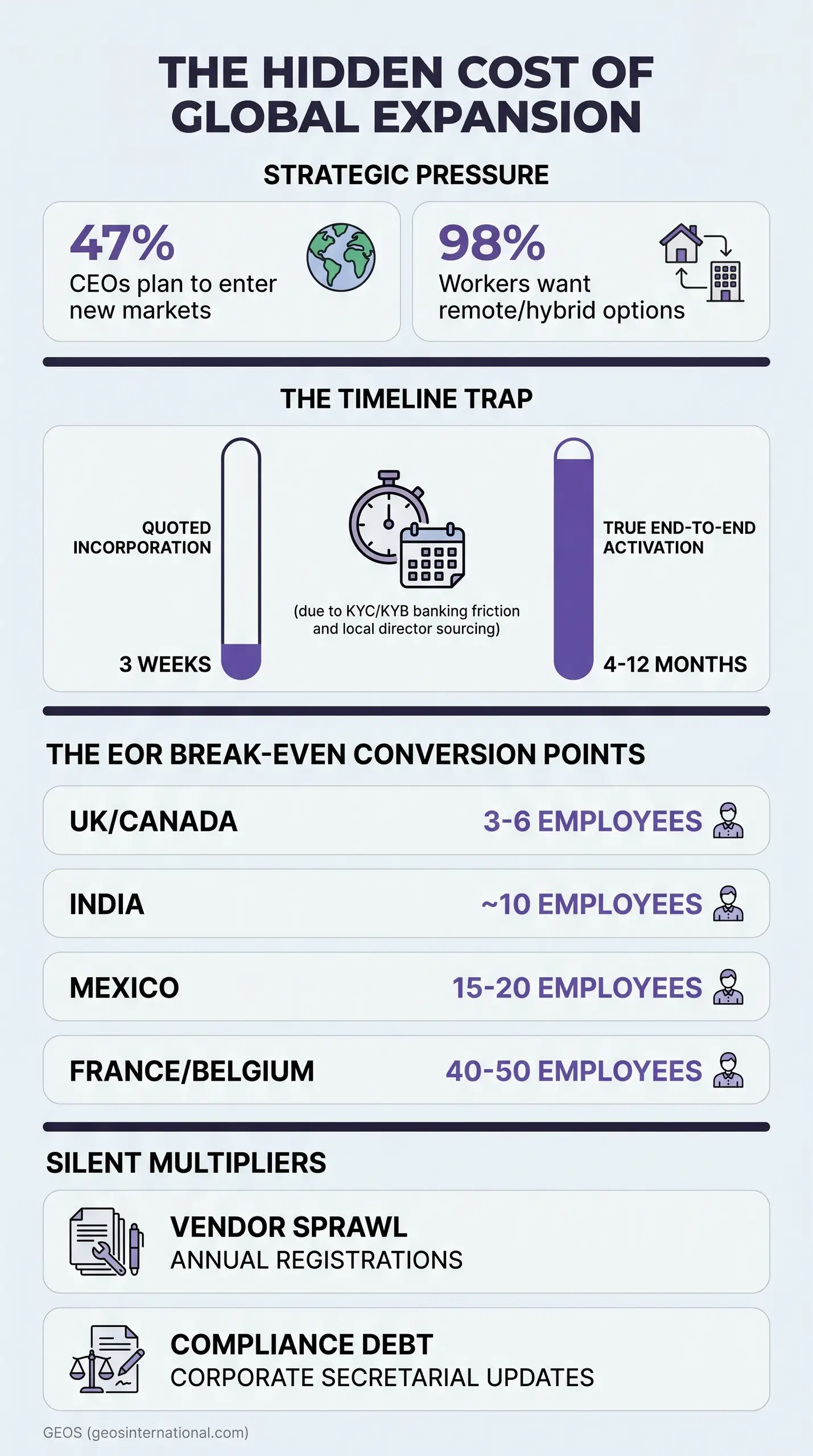

The demand for international expansion is easy to understand. Nearly 47% of CEOs report plans to enter new markets, largely to access talent. Cross-border hiring has also accelerated because roughly 98% of workers say they want remote or hybrid options. The strategic pressure is real. The operating work still needs to be scoped properly.

The First Hidden Cost Appears Before Legal Work Begins

When a founder asks how quickly an entity can be set up in France, Mexico, or India, I usually start somewhere else. I ask why the entity is needed in the first place. I view that discussion as an act of mutual problem solving. The right structure depends on the objective, not on the excitement of planting a flag.

A foreign subsidiary should be treated as a permanent decision. Once it exists, the company owns tax, payroll, employment, banking, corporate secretarial work, and the recurring filings required to keep the lights on from a compliance perspective. That burden starts the day the structure is approved, not the day the company hires its tenth employee.

In practice, there are usually several ways to achieve the same business outcome. If a company only needs to hire one or two employees in Belgium, Brazil, or Japan, I will usually recommend an Employer of Record. If the goal is to build an EU hub, reclaim taxes as an e-commerce business, establish a stronger local commercial presence, or build internal global payroll infrastructure, a direct entity may be the correct path. There are also situations where a company can test local sales activity below VAT thresholds and avoid immediate incorporation.

I also see companies ask about foreign employer registration as a shortcut to direct payroll. In many cases, that creates practical drawbacks without delivering the control of a proper entity. The first hidden cost is choosing the wrong structure. A temporary problem gets solved with permanent infrastructure.

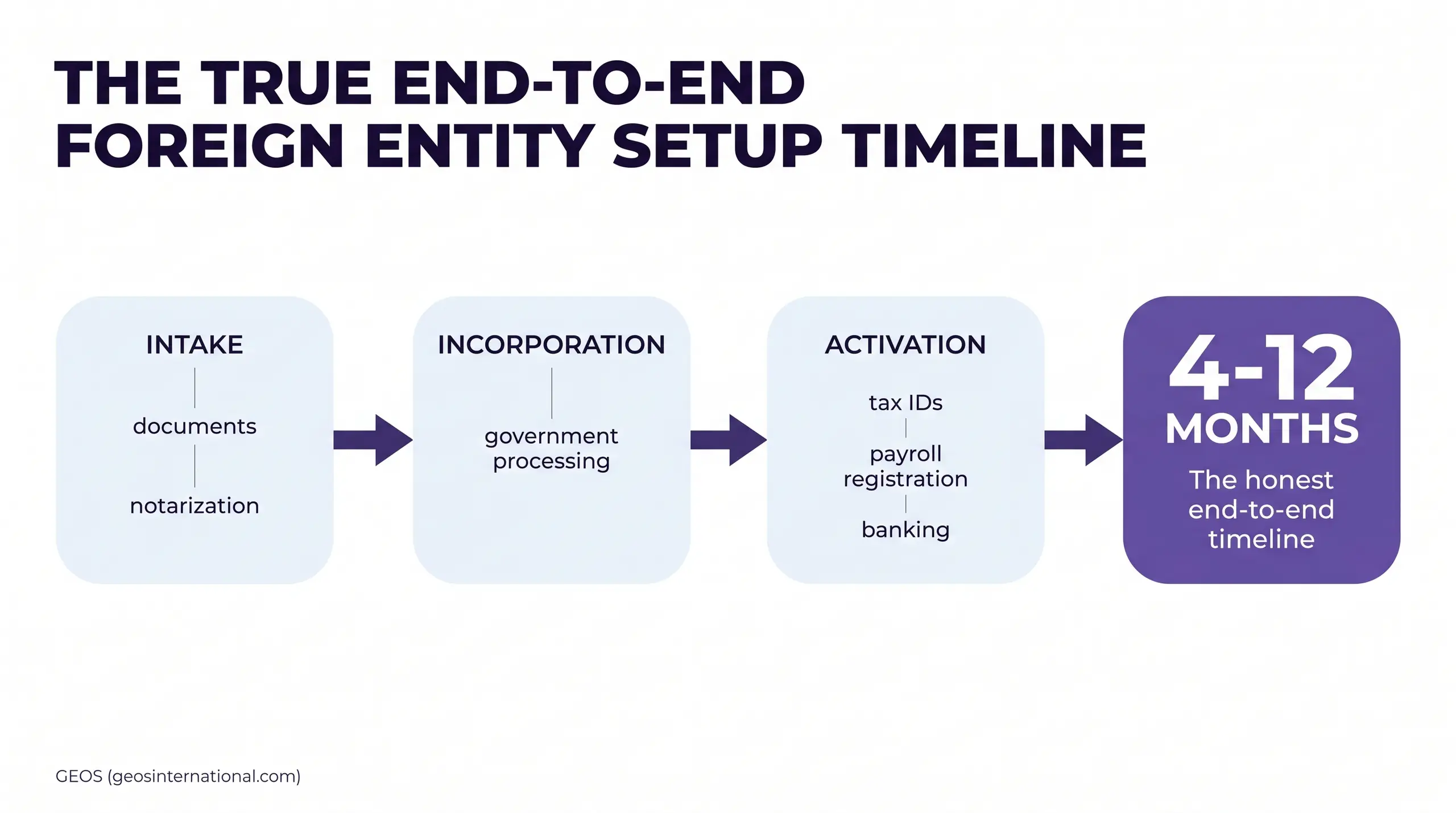

Short Incorporation Timelines Usually Describe the Wrong Thing

One of the most common mistakes in this market is confusing incorporation with activation. A local lawyer quotes three weeks. Leadership hears three weeks to market. Boards build that into planning. In my experience, those short timelines are wrongfully quoted almost every time because they usually describe only government processing time.

The actual project starts much earlier. Parent company documents need to be gathered. Ultimate Beneficial Owner information needs to be collected. Depending on the jurisdiction, documents may then need to be certified, notarized, apostilled, translated, and physically couriered into the country. Germany is a good example, where important parent documents are often notarized, apostilled, and couriered before the core process can move.

The intake stage is often the real bottleneck. I have seen entity launches stall because a shareholder or owner of the parent company was not involved in day-to-day operations and did not want to provide updated proof of address or notarized identification. Local authorities do not treat that as optional. If those documents are delayed for too long, incorporation applications can expire and the entire process may need to restart.

Post-incorporation work is just as important and usually ignored in the early planning. A certificate of incorporation does not mean the entity is operational. Tax IDs may still be pending. Payroll registrations may not be complete. Benefits, social security, and other employment infrastructure may still be missing. A local bank account may still be unresolved.

This is why I prefer to quote the full path to activation, not just the filing date. In many countries, the honest end-to-end timeline is four to twelve months. The UK is one of the faster exceptions, where setup can often be completed in two to three weeks. Most other countries do not behave that way, and founders deserve to see that upfront rather than receive the process piecemeal by email or phone calls.

Banking and Local Representation Are Major Cost Centers

Founders often assume the entity is the hard part and the bank account is administrative follow-through. In many countries, the opposite is true. Setting up a local bank account as a foreign-owned company can be more difficult than incorporating the entity itself.

The issue is straightforward. The company is approaching the bank as a 100% foreigner entering the country. That means full KYB on the parent, KYC on the owners, and scrutiny on the business model, source of funds, and intended local activity. If the jurisdiction requires share capital to be deposited before incorporation is finalized, banking delays can stop the entire project.

Germany illustrates this well. A standard GmbH requires a €25,000 share capital deposit to obtain the certificate that allows the incorporation to proceed. Traditional banks can be difficult with fully foreign-owned companies, which is why I consistently point clients toward more innovative banking options that have workable onboarding protocols. For startup situations, the UG can be a useful alternative because it avoids the need to fund the full share capital upfront.

India and Mexico create different challenges. In India, a company may complete the legal incorporation and still have a meaningful operational runway ahead of it. A traditional local bank account on Indian rails is needed so Tax Deducted at Source remittances and Provident Fund pension payments are actually recognized by local authorities. In Mexico, local social security payments are restricted to a small group of banks, and only one or two are generally workable for foreign-owned entities. Local representation matters there as well. A legal representative may be needed to appear before authorities and wet sign employment contracts, and that role carries real personal liability.

Across many markets, resident directors, nominee directors, or legal representatives are not a minor line item. They are central to market entry. When those individuals take on statutory responsibility, they also take on personal risk. That is why quality and vetting matter far more than cost minimization in this part of the process.

Country Variance Changes the Entire Operating Model

A generic global expansion playbook sounds efficient. In practice, it usually fails because the operational variance from country to country is so large. The right answer in one market can be the wrong answer in the next.

Canada is one of the better examples of a country that looks easy at first glance and still requires informed planning. Incorporation is comparatively fast for foreign owners because the process usually avoids the classic notarization and apostille burden. The practical difficulty often appears later. The Canada Revenue Agency portal is inaccessible to non-residents, so an authorized Canadian representative becomes important for ongoing administration. Structure matters too. I generally advise foreign companies to choose provincial incorporation, such as Ontario, over federal incorporation because federal rules require 25% of the board to be Canadian residents.

France and Belgium often produce the opposite dynamic. If the objective is simply to hire a small number of employees, the effort and cost of direct incorporation can be disproportionate. EOR tends to remain the cleaner answer for longer. If the objective is to build a broader EU hub, countries such as Ireland or some Eastern European jurisdictions may offer a more efficient path, depending on the tax and employment goals involved.

Mexico and India each require a different level of operational preparation. Mexico is document-heavy, with notarized, apostilled, and translated parent company records often moving by courier. Ongoing payroll and accounting also work differently, with compensation calculated more like a day rate than an annual salary. India can be relatively straightforward at the incorporation stage and then become complex afterward, with resident director requirements, powers of attorney, local banking, and mandatory registrations. This is why country selection should be treated as an operating decision, not just a market opportunity decision. It is the same logic behind the Global Subsidiary Index.

EOR Is Valuable, but It Has a Clear Conversion Point

I am not anti-EOR. I spent enough time in that market to understand why it grew so quickly. The value proposition is real. Industry data suggests companies can save roughly 4 months of setup time by using an EOR instead of launching a subsidiary. Providers also typically charge around 10 – 15% of monthly gross salary as a service fee. At low headcount, that tradeoff often makes sense.

The reach is also compelling. Major EOR platforms can support hiring in 180+ countries. That scale explains why many growth companies default to the model. It solves a real problem at the beginning of the global expansion journey.

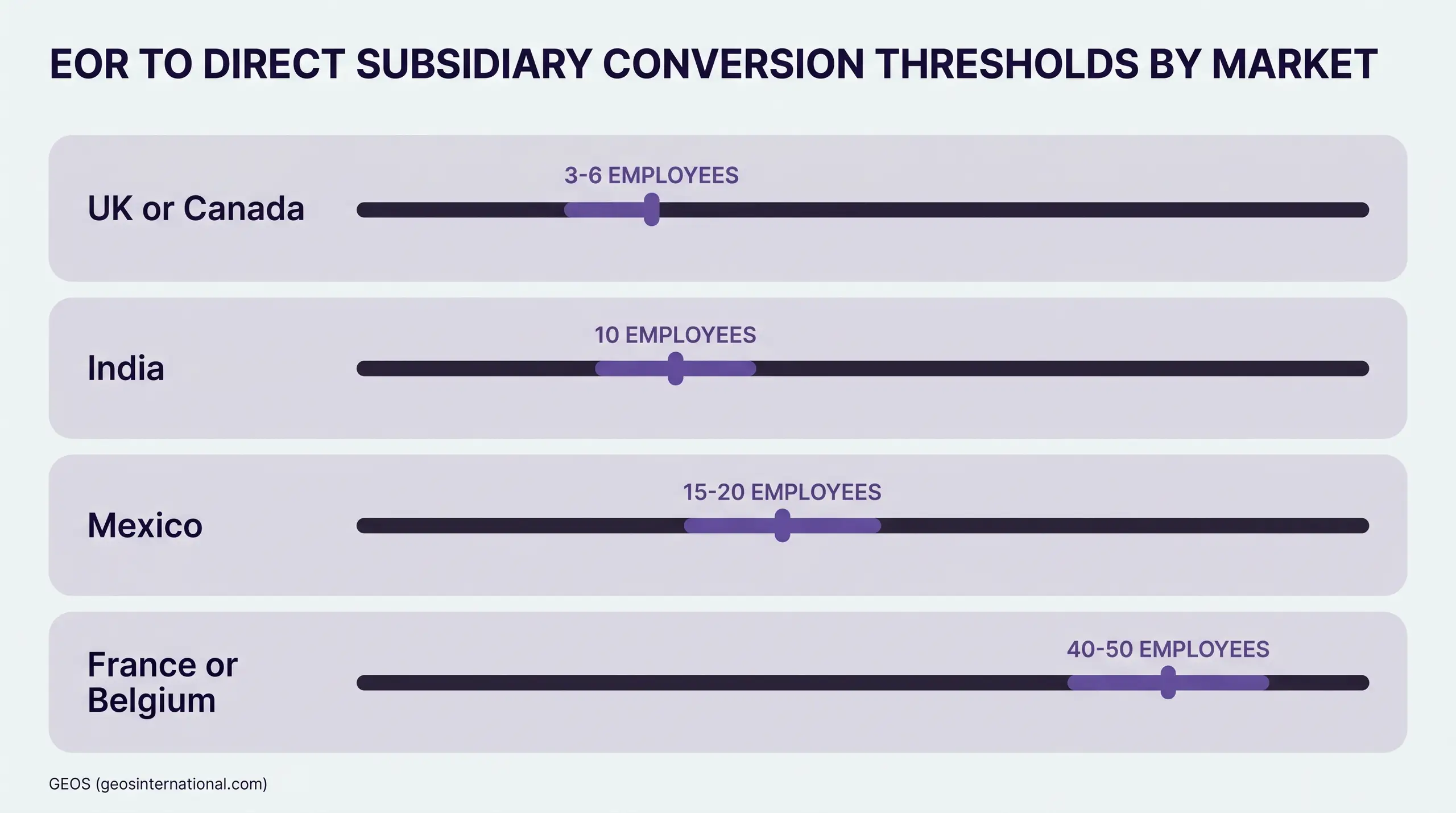

The issue starts later. EOR is most useful at the beginning, and sometimes through the middle, of a company’s international growth. It becomes less efficient once the company has reached critical mass in a country. At that point, the monthly service fee compounds, local control remains limited, and the company starts to lose the benefits that come with having its own establishment.

The break-even point varies sharply by market. In the UK or Canada, the shift can happen around three to six employees. In India, it is often around 10, especially when the company intends to scale a larger local team or run a global command center. In Mexico, the threshold is more commonly fifteen to twenty employees. In France or Belgium, where direct setup and maintenance are heavier, the threshold can be closer to forty or 50 employees.

There are also strategic reasons to convert before the pure cost math becomes obvious. A direct entity gives the company more control over benefits, HR rules, and equity grants. It can strengthen local credibility and support direct contracting with enterprise or government customers. In some countries, regulation forces the question earlier. Germany’s AUG framework, for example, limits EOR usage to 18 months and then requires a three-month break if the company does not establish its own structure.

The legal risk is also more nuanced than many founders assume. EOR firms do not absorb all liability on behalf of the client. The contracts usually create shared liability, and local scrutiny can increase quickly after an unsavory exit or another employment issue. Permanent establishment concerns can also start to surface once a company is carrying meaningful headcount through an EOR, often in the range of five to twenty employees depending on the country. For serious labor and employment violations, industry data often cites exposure of up to 10% of global turnover.

The transition itself has hidden costs as well. The most difficult part is often not the entity incorporation. It is the legal continuity of moving employees off the EOR and onto the new local company. Employment contracts need to be issued properly, accrued entitlements need to be addressed, and communication with employees has to be handled carefully. A sound conversion requires entity setup, employment infrastructure, transfer planning, and a new HR playbook for the local entity.

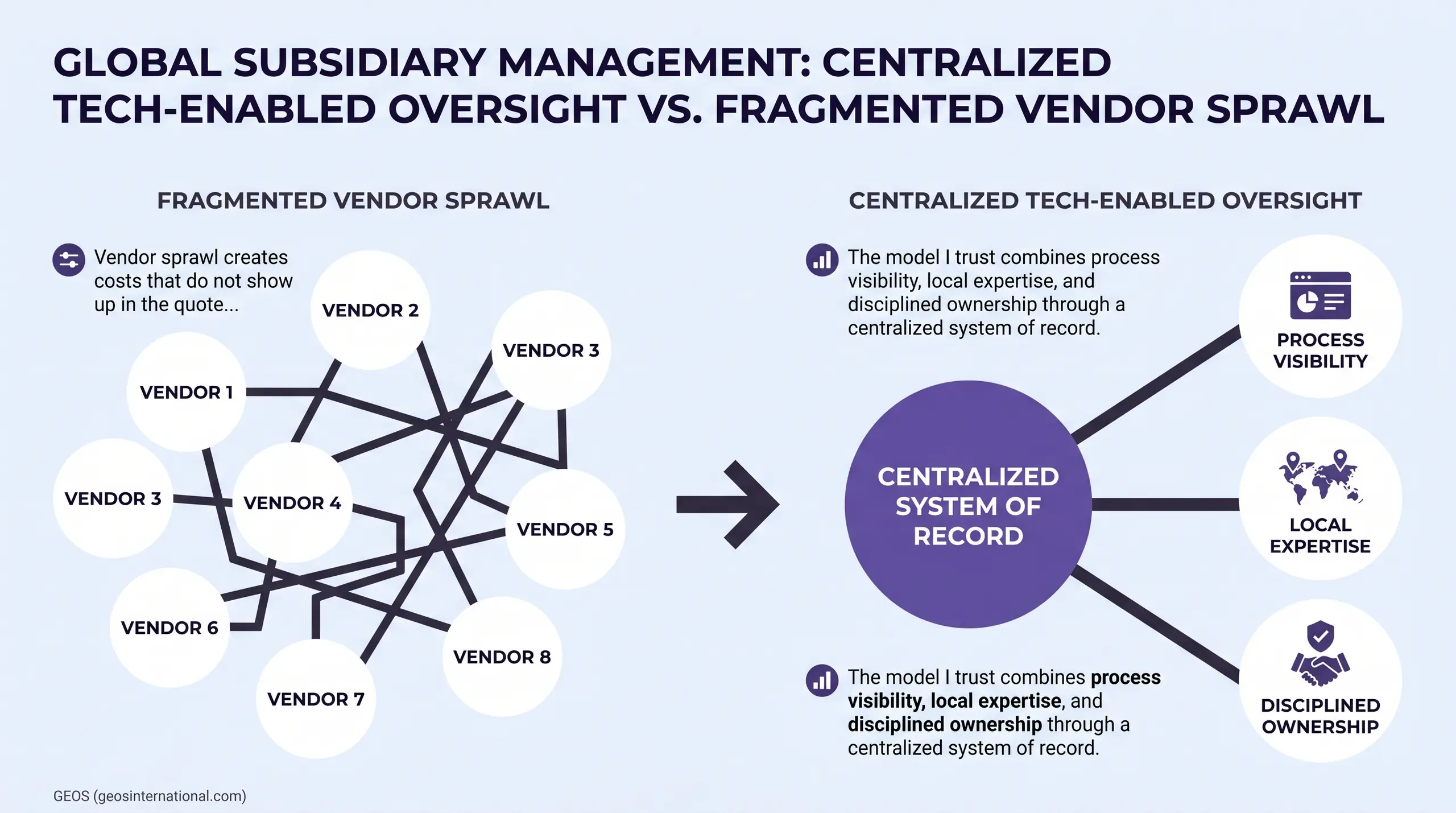

Vendor Sprawl Creates Costs That Do Not Show Up in the Quote

Many companies respond to this complexity by going to one of two extremes. They hire a low-cost local lawyer or accountant in each country, or they retain a global consulting conglomerate. Both approaches can work in limited cases. Both also create hidden administrative cost.

Single-market local providers are often the cheapest line item. They are rarely the cheapest operating model once a company expands beyond one or two jurisdictions. The process is commonly a black box in terms of the steps that need to be taken. Fees can expand, communication can slow down, and hourly billing can end up incentivizing dependency. Foreign parents also run into a practical issue: many local firms do not regularly work with foreign-owned companies and underestimate what cross-border setup actually requires.

Large global firms solve some of the local expertise problem, but they introduce another one. Their teams are fragmented by region, so the client keeps repeating context, resubmitting the same parent company materials, and coordinating multiple workstreams under one logo and one umbrella. In practice, the client still ends up owning the project management from beginning to end while also paying for significant overhead. That model remains expensive, bloated, and stuck in the past.

I have seen both patterns firsthand. GEOS helped one client move four global subsidiaries away from a Big Four firm by giving them a clearer operating model and more transparent pricing. We also worked with a company that had more than 30 international entities and had effectively lost visibility into compliance costs because local firms were invoicing the subsidiaries directly. Untangling that situation required a dedicated full-time internal hire alongside our team. Once a company has more than a handful of entities, vendor sprawl starts to look like a staffing issue, not just a procurement issue.

Compliance Debt Builds Quietly and Then Arrives All at Once

Corporate secretarial work varies by country, but at a high level it is the function responsible for keeping the lights on from a compliance perspective. Annual registrations, director updates, registered address changes, extra-provincial registrations, VAT-triggered obligations, and last mile tax filings all sit in that layer. If those items are managed in spreadsheets and scattered inboxes, something eventually gets missed.

We saw that directly in Peru. A former employee had been left in place as the legally required second shareholder. Once that person departed, the entity was left with only one shareholder and fell out of good standing. Our team had to move quickly to draft the required documentation, appoint a replacement shareholder, and restore compliance. The legal issue looked narrow on paper. The operational risk was significant.

Without a centralized system of record, global subsidiary management starts to feel like playing with a blindfold. Leadership teams receive information piecemeal by email or phone calls and then spend time trying to play catch up in terms of what was missed. The direct cost may be a filing fee or a remediation invoice. The larger cost is management distraction and the loss of confidence that follows.

The Operating Model I Trust

The model I trust combines process visibility, local expertise, and disciplined ownership. Technology should be an enabler. It should organize documents, map the workflow, issue notifications, and act as more of a connector between the client team and local experts. It should not pretend that AI can complete incorporations on its own while the underlying work still depends on public notaries, wet signatures, manual registrations, and bespoke government portals.

That is why our own AI assistant, Geovanna, is intentionally limited. It can answer questions based on verified content and a client’s entity data. It does not carry out incorporation work. Human expertise is still required on the ground, and human communication still matters. A platform should sit alongside standing meetings, Slack channels, and direct service, not replace them.

The same principle applies after launch. For existing entities, the right process starts with intake, document collection, and mapping the known compliance obligations in each jurisdiction. It then adds the client-specific items, such as VAT registrations or payroll-related tasks, and assigns ownership across internal teams and vendors. Where an incumbent local provider is strong, I am comfortable keeping them in place. Where they are weak, I prefer to fortify that with pre-vetted vendors or replace them entirely. The key is that the parent company finally has oversight.

The Questions I Settle Before a Company Launches

Country

The first question is where the entity should be formed, and why that specific jurisdiction is the best option. Sometimes the answer is obvious. Sometimes a neighboring market can deliver the same commercial or employment outcome with a much cleaner setup and lower maintenance burden.

Objective

The second question is the real purpose of the entity. Hiring a few employees, reclaiming tax, signing local contracts, opening a local office, or building an EU hub all lead to different structures and different timelines. If the objective is vague, the budget and delivery plan will be vague as well.

Infrastructure

The third question is operational. Which owners will provide KYC documents? Who will handle payroll, accounting, benefits, and CorpSec? How will banking be approached? If those dependencies are unresolved at the start, the company is effectively funding delay before the project even begins.

Final Thought

Foreign subsidiaries can unlock better economics, stronger employment control, and the legal standing to sell locally at scale. I believe in moving quickly, and I also believe in sustainable infrastructure. GEOS is bootstrapped, and that has reinforced the same discipline I recommend to clients.

The hidden cost in foreign subsidiary setup is rarely the initial legal fee. It is the combination of poor structure choice, incomplete timelines, banking friction, vendor fragmentation, and compliance debt that surfaces later. Companies that handle expansion well make the full process visible from the start, choose the right tool for the stage they are in, and build enough operating discipline to support the entity after it goes live. That is how international expansion stays ambitious without becoming chaotic.

Frequently Asked Questions

What is the actual financial risk of stretching our EOR usage instead of establishing a permanent subsidiary?

The legal exposure is severe. EORs do not shield you from permanent establishment risks if your local team generates revenue. For serious labor and corporate violations, industry data highlights penalties reaching up to 10% of global turnover. You are risking your capital on avoidable compliance failures.

Can we bypass the 4-12 month activation timeline by purchasing a dormant local shelf company?

It sounds like a cheat code, but it rarely accelerates your timeline. You inherit the entity’s historical compliance debt, and local banks will still require full KYC and KYB on your parent company to unlock existing accounts. It is often a messier, more expensive path than disciplined incorporation.

How does a direct foreign subsidiary improve our ability to grant equity to local top-tier talent?

It fundamentally shifts your leverage. EORs restrict your ability to grant true stock options, forcing you into phantom equity workarounds. A wholly owned subsidiary allows you to implement localized, tax-advantaged ESOP pools directly, giving you the operational control needed to aggressively out-compete local tech giants.

What is the most efficient way to inject our Series B capital into a newly formed foreign subsidiary?

Do not simply wire funds as intercompany revenue. You must establish formalized intercompany agreements – usually via direct equity injections or formal loan facilities – to avoid triggering massive local tax events. Transfer pricing rules apply immediately. Finalize this capitalization strategy before you ever fund the local bank account.

Does operating through a local foreign subsidiary actually shorten regional enterprise sales cycles?

Absolutely. Enterprise and government procurement teams despise cross-border vendor risk. A local subsidiary provides a domestic tax ID, localized data processing agreements, and the ability to invoice in the local currency. It eliminates the friction of international contracting, turning your legal infrastructure into a revenue-enabling asset.