I think about subsidiary management as a control problem. At its core, it is an act of mutual problem solving between the parent company and the people helping it expand. The finance team is trying to support growth in new markets without losing control of cost, compliance, or accountability.

For a long time, the default answer has been a spreadsheet supported by local accountants, lawyers, and long email threads. That approach creates a sense of order for a while. Then the business adds a few more entities, a few more vendors, and a few more jurisdictions. The spreadsheet remains, but the operating model starts to slip.

I co-founded GEOS after working across healthtech, capital markets, global payroll, and EOR, and after seeing how painful global entity setup and management still are. I have also been the client of large legacy Big 4 firms. The consistent issue is visibility. Information is still received piecemeal by email or phone calls. Many providers still operate as if they are a black box. That is a poor fit for any CFO who needs clear ownership and predictable outcomes.

The spreadsheet problem

Low cost on paper, high cost in practice

The external environment is getting harder, not easier. In a recent survey, 85% of companies said compliance requirements had become more complex over the last three years. At the same time, 63% cited disaggregated data as a major reason compliance is difficult. The business impact is broader than legal or tax. 77% of companies said that complexity had already affected five or more growth-driving areas.

Those numbers track closely with what I see in practice. Complexity is rising while the underlying information is still spread across inboxes, PDFs, local portals, and spreadsheets. That gap matters more every quarter.

The spreadsheet model usually fails quietly. First, a deadline gets pushed because a local provider is slow to respond. Then an invoice arrives that no one can validate. Then someone realizes a foreign subsidiary has been billed directly for months, outside the normal approval flow. I worked with a company managing more than 30 entities where this had gone on long enough that they hired a dedicated person just to untangle the global compliance picture. Even with that hire, the situation still required years of backdating, auditing, and cleanup. The problem was not effort. The problem was fragmentation.

Once a company has more than a handful of entities, vendor management alone can become the equivalent of two or three full-time jobs. That is before anyone improves the process itself. In that environment, the spreadsheet becomes a record of last known information. It does not function as a reliable control layer.

Hidden risk sits inside the gaps

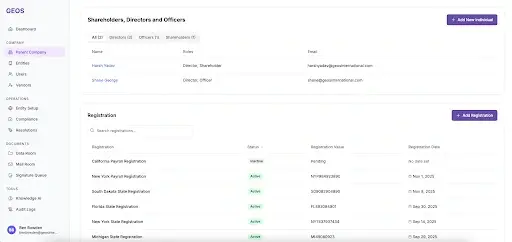

A finance team also needs to separate “incorporated” from “operational.” Spreadsheets rarely do that well. A row may show that an entity exists in France, Mexico, or Singapore. It usually does not show whether the tax ID is active, whether payroll can run, whether the bank account passed KYB, whether a resident director is in place, or whether annual filings and local registrations still match the way the business is operating.

That distinction matters because many entity problems sit dormant for a long time. One example stays with me because it shows how hidden these issues can be. When my team onboarded a client’s entity in Peru, we found that the structure no longer complied with local shareholder rules. The entity needed two shareholders. One of them had been a former employee who had left the business a couple of years earlier. The entity was at risk of falling out of good standing because the paperwork had never been updated. We moved quickly, aligned with the client on a replacement, drafted the documents, and restored compliance. None of that was obvious from a simple status file saying the entity was active.

The same lack of visibility shows up during setup. Timelines are wrongfully quoted almost every time because many providers quote only the narrow government processing window. That leaves out the real work. Parent company documents still need to be collected. Directors and UBOs still need to provide IDs and proof of address. Documents may need to be notarized, apostilled, translated, and couriered. Foreign bank KYB can be harder than incorporation itself. In the UK, setup can often be done in two to three weeks. In most other markets, a realistic setup timeline is closer to four to twelve months when the full process is included. Finance teams get hooked into a false promise when that distinction is ignored.

The volume of change alone should make teams cautious about relying on manual trackers. Thomson Reuters Regulatory Intelligence reported an average of 246 new regulatory alerts per day worldwide. A workbook cannot absorb that kind of movement across countries, vendors, and filing regimes.

The usual alternatives still leave gaps

The single-market black box

Once the limits of spreadsheets become clear, many companies move to single-market local accountants or lawyers. That is often the lowest-cost option. It can work in one country if the use case is narrow and the internal team has time to manage it closely.

The issue is scale and transparency. These firms usually only work in their own market. They often bill by the hour. They often have limited incentive to share a complete picture with a foreign parent company. In practice, that model can end up incentivizing dependency. Each step is often a surprise on what comes next. The finance team knows its home-country rules well. It does not know what it does not know in every jurisdiction.

That information asymmetry is the real problem. Local vendors may be competent. The client still lacks a way to verify what is happening across multiple countries, multiple filings, and multiple partners. Once that setup expands beyond one or two markets, the black box becomes a structural issue.

The legacy safety premium

The other common path is to default to a global consulting or accounting brand. I understand why CFOs are drawn to that. These firms have tax, legal, and compliance resources across many jurisdictions. On paper, it looks safer.

In practice, the service model is often fragmented by region. The client still has to onboard with separate country teams, repeat the same parent company context, and manage internal borders inside the vendor. The work is still rooted in manual processes. The price is materially higher.

I saw this clearly with a company managing four subsidiaries globally through a large incumbent in the space. When we showed them the GEOS platform and our pricing, the reaction was immediate. They saw the benefit of having one system that gave them direct visibility into the compliance position of each entity. They also saw how much cost and complexity had been hidden in the old model.

That cost base matters. A 2016 analysis estimated an average carrying cost of about US$50,000 per entity per year when legal, tax, and secretarial work are handled properly. Finance leaders should know where that spend goes. Paying for bloated overhead without getting clear control is difficult to justify.

EOR and entity ownership are part of the same journey

When EOR is still the right tool

A lot of finance teams hit the subsidiary management issue when they start out with an Employer of Record and then scale beyond it. I want to be precise here. I do not view EOR as a trap. I spent time on that side of the market, and I still believe it is one of the most useful tools for early global hiring.

For a company hiring its first employee, or its first small group, in a market, EOR is often the right answer. It is usually faster, safer, and more practical than trying to hire a foreign full-time employee as an independent contractor. It is also often the best way to validate a market before standing up permanent infrastructure.

This is why I think of global expansion as a journey that has a beginning, middle, and end. EOR plays an important role at the beginning and often through part of the middle.

When a company has reached critical mass

The economics and risk profile change once a company has reached critical mass in a country. In the UK or Canada, the financial break-even for moving from EOR to an owned entity can be around three to six employees. In France or Belgium, the break-even can be much higher because local setup and maintenance are more involved.

Permanent establishment risk follows a different curve. Depending on the country, companies can start to attract scrutiny when they have roughly five to twenty employees in one market through an EOR. The threshold is country-specific, but the pattern is consistent. At some point, the monthly fee stops making sense and the control gap becomes harder to defend.

At that stage, the return on an owned entity is broader than monthly savings. The company gains more control over benefits, equity, and local HR rules. It may unlock tax advantages. It may be able to contract locally, sign leases, or sell to enterprise and government buyers that expect a local presence. Some companies need an EU hub. Some e-commerce companies need local infrastructure to reclaim taxes. Some are building their own internal EOR function. The right answer depends on the business objective, but the decision should be made deliberately.

The transition itself needs more discipline than most teams expect. The hardest part is usually not incorporation. It is legal continuity for employees. People need to move from the EOR’s contract to the company’s own local contract without confusion around payroll timing, seniority, vacation accrual, private pensions, benefits, work permits, or social insurance. In practice, I treat EOR-to-entity conversion as a sequence. First, the entity and local infrastructure have to be set up. Then the employment framework has to be built. After that, the transfer has to be planned with the EOR and communicated properly to employees. Only then should the new entity run payroll and begin operating as the direct employer.

That sequencing matters because EORs do not absorb all of the underlying risk. Most contracts are built around shared liability. If an employee relationship ends badly, or if local authorities review how the team is operating on the ground, the parent company is still in scope. An unsavory exit can bring the whole arrangement under closer scrutiny.

What modern subsidiary management requires

A real system of record

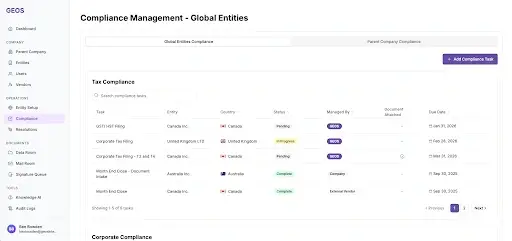

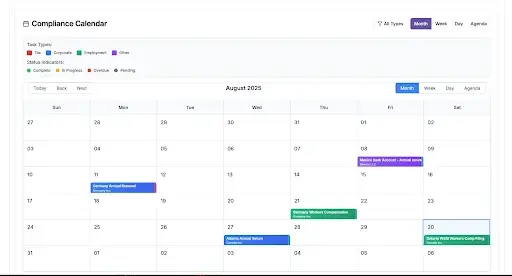

Moving beyond spreadsheets requires more than a better tracker. It requires a true system of record. Every entity should have a clear profile. That includes the legal structure, registrations, documents, ownership details, deadlines, service providers, and audit trail. The same system should show which tasks are due, who owns them, and whether they have been completed.

A large share of entity management is simply keeping the lights on from a compliance perspective. That includes annual registrations, director and shareholder changes, board resolutions, registered address management, and other corporate secretarial work that has to be done on time in every country. A system of record should make that work visible.

Better coordination has a measurable effect. 59% of compliance leaders report greater confidence in decision-making when compliance processes are better coordinated. And PwC Global Compliance Survey 2025 found that 71% of companies are planning significant digital transformation initiatives and 82% plan to increase investment in technology to automate compliance and reporting. Finance leaders are moving in this direction because they want fewer blind spots, not because technology is fashionable.

That is the principle behind GEOS. We spent hundreds of hours mapping the setup and management workflows for more than 80 countries. We did that because there are no shortcuts in this category. The workflow has to be mapped in detail before software can improve it.

When we migrate an existing footprint onto the platform, the process starts with disciplined intake. We gather the entity documents, organize them, build the entity page, map the country-level compliance tasks, and then layer in the client-specific items such as VAT registrations or payroll obligations. We also ask who the existing vendors are and assign the right tasks to them inside the platform. That matters because many issues only surface once the information is finally assembled in one place.

The pricing model should reflect the same reality. Not every entity needs the same level of support. In our own model, a finance team may use Access at $49 per entity per month when it mainly needs a global system of record. It may apply Core or Core+ only in the countries where active corporate secretarial support, Slack integration, or dedicated account coverage are required. That modularity is more realistic than forcing the same service level across every jurisdiction.

Technology with human guardrails

There is a realistic way to think about AI in this category. I do not believe fully automated entity setup is possible in 99% of countries today. Public notaries, government portals, physical courier, bank requirements, last mile tax filings, and local legal steps still require people on the ground. The process is still heavily rooted in manual processes.

PwC Global Compliance Survey 2025 also found that 71% of companies expect AI to have a positive impact on compliance and 46% are already using it for compliance tasks. I agree with the direction. I do not agree with the myth that AI can replace localized execution in a process that still depends on local humans.

That is why our own AI assistant, Geovanna, is limited by design. It helps clients retrieve information about their own entities and ask common questions quickly. It does not execute incorporation or compliance tasks. That guardrail is deliberate. The same logic applies to resident directors and similar roles. In markets where a local individual must take formal responsibility, that person is taking real legal liability. The work demands human judgment, a pre-vetted network, and clear accountability.

The practical benefit for finance is simple. Foreign tax notices can be scanned into the platform, tied to the right entity, assigned to the right owner, and pushed into Slack instead of disappearing into physical mail.

Oversight across local partners

A modern model also has to account for reality. Most companies already have some local partners they trust and others they do not. The answer is rarely a full rip-and-replace.

In practice, a company may keep a strong provider in Canada and Mexico while replacing a weak setup in Singapore. The platform should support both. Its role is to create oversight. It should map what compliance should look like in each country, compare that against what local partners are actually doing, and fortify that with pre-vetted vendors where a gap exists.

That oversight layer is one of the most important changes finance can make. It removes blind trust. It also reduces the dependency that traditional local providers often rely on.

A practical operating standard for finance leaders

Start with the business objective

When I advise founders and finance leaders on expansion, I start with three questions. Which country is the target. Why is the entity needed. What infrastructure and partners already exist to support it.

Those questions sound basic. They determine almost everything. A company opening a French entity to hire three employees may be better served by an EOR. A company entering Mexico to sign contracts, build a local team, and establish tax infrastructure is in a different position. There are often five to seven ways to reach an international objective. Entity setup is only one of them.

Some companies can test a market through local sales activity without crossing VAT thresholds. Others can start with contractors or an EOR and wait until there are multiple concrete reasons to incorporate. The operational question I care about most is simple: how difficult and how expensive is it to set up and maintain the infrastructure required for the actual goal in that market.

Build sustainable control early

For finance teams that already have a global footprint, the priority is to centralize before the complexity grows again. I generally prefer a B-plus plan executed today over an A-plus plan next week. In this context, that means getting the system of record, document management, compliance calendar, and vendor accountability in place now, rather than waiting for a perfect redesign later.

That maturity gap is still wide across the market. Only 7% of companies consider themselves leaders in compliance maturity. Most organizations are still operating with more international complexity than their infrastructure can support.

The practical standard is straightforward. The finance team should be able to open one system and understand the status, cost, owner, and next action for every entity.

Closing

Subsidiary management has moved beyond the point where spreadsheets can serve as the operating backbone. They are fine as a scratch pad. They are weak as a control framework for a multi-country structure with legal, tax, employment, and corporate secretarial obligations. At a certain scale, the business is effectively playing with a blindfold.

The teams that handle this well do a few things consistently. They centralize data and documents. They make ownership visible. They use technology to organize the work, not to pretend the work is fully automated. And they keep local expertise close to the process.

That is how a global footprint becomes manageable. It is also how finance leaders regain confidence that the business is expanding with control rather than simply expanding with hope.

Frequently Asked Questions

What is the true annual carrying cost of maintaining a foreign subsidiary?

Budget heavily for overhead. A TMF Group analysis estimates foreign subsidiary carrying costs at US$50,000 annually, encompassing legal, tax, and secretarial maintenance. CFOs must map this predictable baseline against Employer of Record fees to calculate precise mathematical break-even thresholds.

How does disaggregated entity data directly impact a scale-up’s growth trajectory?

Fragmented data creates severe operational bottlenecks. According to PwC, 63% of companies say disaggregated data complicates compliance, and 77% report this complexity harms five or more growth areas. Hidden liabilities in isolated spreadsheets inevitably delay market expansion, fundraising, and audits.

How can finance leaders track global regulatory shifts without hiring dedicated local compliance teams?

Deploy a centralized system of record. Thomson Reuters tracked an average of 246 new regulatory alerts globally every day. Manual trackers cannot absorb that volume. Replacing fragmented inboxes with automated dashboards ensures critical statutory deadlines are flagged instantly, mitigating permanent establishment risk without inflating headcount.

Can CFOs consolidate foreign compliance oversight without firing their trusted local accounting vendors?

Yes, through a vendor-agnostic oversight layer. You rarely need a full rip-and-replace. Modern compliance platforms let you onboard preferred single-market accountants into one unified dashboard. This establishes strict accountability, maps what local partners are actively executing, and instantly flags surprise billable hours or missed deadlines.

Why are risk-averse CFOs aggressively prioritizing compliance technology over legacy consulting firms?

Legacy firms operate as expensive, fragmented black boxes. To regain control, 82% of organizations are increasing tech investments to automate compliance. Centralized platforms eliminate information asymmetry, allowing finance executives to oversee multi-country structures directly, reduce bloated advisory retainers, and ensure total audit readiness.