Mexico is an attractive market for foreign expansion. It offers depth in talent, strong commercial ties, and meaningful long-term opportunity. It also has one of the more demanding operating environments for a foreign-owned subsidiary.

Most finance leaders know tax and compliance deeply in one jurisdiction: their own. Once a company expands abroad, that certainty drops quickly. Mexico can look manageable at first because the legal incorporation step is often presented as a short project. In practice, the real work sits around the filing. The risk comes from omitted steps, weak local controls, and a model that looks cheaper than it is.

I co-founded GEOS after seeing this from several angles. I had already worked through the EOR model, then through traditional entity setup with large advisory firms, and then into building a platform for global subsidiary management. The lesson was consistent. Incorporation is only one slice of the problem. Banking, tax registration, payroll, local representation, and ongoing corporate secretarial work determine whether the entity becomes useful or simply expensive.

Start with the business objective

I approach subsidiary setup as an act of mutual problem solving. The first question is simple: why does the company need Mexico now? Hiring, local revenue, enterprise contracting, tax planning, local reputation, and office infrastructure each lead to a different answer.

In many cases, the right first step is not a subsidiary. A global expansion journey has a beginning, middle and end. If the business is hiring its first few employees, an Employer of Record can be a sensible bridge in Mexico. That country is complex from an employment and payroll standpoint, so the point where an owned entity creates better economics is usually later than in places like the UK or Canada.

In my experience, Mexico often requires closer to fifteen to twenty employees before the economics clearly justify going direct. That threshold can move earlier if the company is also generating meaningful local revenue, needs a permanent establishment for contracts, or has a tax reason to build local infrastructure. Headcount matters, but it is only one variable in the decision.

The shortcut I would avoid is aggressive contractor classification. Companies often try to save time by treating full-time workers as contractors while managing them like employees. That is a poor control decision in any market, and it is particularly risky in Mexico. A legal guide on recent REPSE enforcement describes a $2.5 million fine issued to a U.S. tech company for worker misclassification. For early hiring, EOR is usually the safer path. It is far more defensible than a contractor structure that does not match reality.

Why Mexico timelines are wrongfully quoted

The filing clock starts after the hard work

Mexico timelines are wrongfully quoted almost every time because many providers start the clock after the parent company has already done the difficult intake work. Official guidance often refers to a 2 to 4 week incorporation process. That can be directionally true for the legal filing itself. It is incomplete for a foreign parent.

Before the filing even begins, parent-company records, director information, and ultimate beneficial owner documents need to be collected and checked. In Mexico, formation documents must be in Spanish. For a foreign parent, that typically means certified translation, notarization, apostille formalities, and physical couriering. None of that is theoretical. It is often what actually determines the timeline.

I have also seen speed collapse for a simpler reason. A parent-company director or UBO delays a notarized ID or proof of address. Local applications expire. The process then has to be restarted. That sounds minor on paper. Operationally, it can shift a quarter.

Banking can add another layer. In some markets, foreign bank KYB is harder than the incorporation filing itself. Mexico is often in that category. A company can be legally incorporated and still have no usable bank account, no payroll capability, and no practical path to go live.

Incorporation and operational readiness are different milestones

This distinction matters because finance teams usually budget against an operating outcome, not a legal certificate. Once the entity exists on paper, there is still work to do. Tax registrations, payroll setup, employment documentation, local benefits, registered address arrangements, and internal approvals all sit downstream of incorporation.

That is where many projects start to drift. The original quote covered one event. The business expected a functioning subsidiary. The missing steps arrive later, often received piecemeal by email or phone calls, and the finance team has to play catch up in terms of what was missed.

At GEOS, we include those pre-incorporation and post-incorporation steps when we scope a project because a narrower quote is not useful for decision-making. A board does not care whether a filing was technically accepted if the entity still cannot hire, pay, sign, or operate.

The Mexican bottlenecks that drive risk

The local legal representative is a core control point

A local legal representative in Mexico is not an administrative checkbox. This individual is a core part of the control environment. They represent the subsidiary before local authorities, often support tax interactions, and may need to wet sign employment contracts for local hires. If that person is weak, poorly vetted, or inactive, the parent company carries the operational consequences.

This is why I am cautious with low-cost arrangements around resident directorship or local representation. These roles carry real personal liability. They should be filled through a pre-vetted network with clear accountability. My co-founders and I have spent more than a decade in the global expansion space, and a large part of that experience has been learning which local relationships actually hold up under pressure.

We have already seen what poor local governance creates in Latin America. In one case, we audited several entities where prior nominee directors had become inactive, leaving the client exposed and out of compliance. In another case in Peru, we had to restore good standing after discovering a departed shareholder had left the entity with only one shareholder instead of the legally required two. Those situations are fixable. They are also avoidable.

Banking and payroll are the real operational gate

Banking is where many Mexico projects stall. The core challenge is access to the actual rails to make the social security payments. Mexico's IMSS authorizes only six banks to receive employer IMSS and INFONAVIT contributions. In practice, only one or two are typically workable for foreign-owned entities. That is a narrow lane.

I have seen companies arrive halfway through the process with a legal entity in place and still no ability to run payroll. They assumed a fintech workaround or a simple transfer structure would solve it. It did not. We had to untangle those situations and start from scratch. This is one reason why established local banking relationships matter so much in Mexico.

The payroll model itself is also more complex than many foreign teams assume. Statutory employer contributions can add about 25 to 35% to gross salary on top of wages. INFONAVIT alone requires a 5% of salary contribution paid every two months. On top of that, payroll in Mexico is calculated more like a day rate than a simple annual salary model. That changes how teams need to think about budgeting, accruals, and monthly accounting.

The administrative layer is still very manual. Mexico's IMSS system still supports payment submission by floppy disk, CD, or USB upload. That detail sounds dated because it is dated. It also explains why I say this space remains rooted in manual processes. Software helps. Local expertise remains essential.

The cost model most finance teams underestimate

Ongoing compliance is broader than tax

The common comparison is monthly EOR fee against one incorporation fee. That framing is too narrow. The better comparison is EOR fee against the full cost of establishing and maintaining local infrastructure.

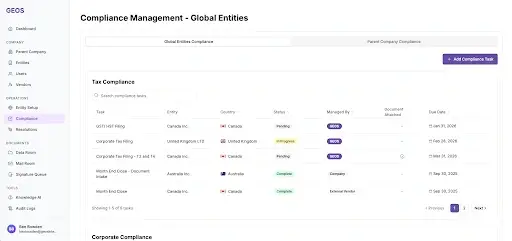

That maintenance layer is broader than many finance models assume. Corporate secretarial work alone is often missed. Broadly, CorpSec is the function that keeps the lights on from a compliance perspective. It covers annual registrations, routine governance filings, document control, and the corporate changes that happen after formation. In Mexico, that sits alongside bookkeeping, annual tax work, VAT or nil filings where relevant, payroll administration, registered address support, and local legal representation.

There is also internal overhead. Once a company has several entities and several local providers, the management burden starts to look like a real headcount problem. I have seen organizations lose complete visibility into compliance costs because local firms were invoicing subsidiaries directly. One client with more than 30 international entities needed a dedicated full-time hire working alongside GEOS just to untangle the backlog and rebuild control. That is what happens when the footprint grows without a system of record.

Mexico's EOR break-even point is usually higher

Because Mexico has heavier employment, payroll, tax, and banking complexity, the ROI line for going direct is higher than many teams expect. I generally see the economics become more compelling around fifteen to twenty employees. That is the range where a company can usually justify going direct and getting a better ROI, assuming it also has the operating support to run the entity properly.

That does not mean EOR removes all exposure. EOR agreements often allocate liability back to the client when the client's own conduct causes the issue. An unsavory exit can also bring the structure under scrutiny. EOR is useful, especially in Mexico. It is usually the best tool early in the journey. It becomes less attractive once the local team has reached critical mass or the business needs the benefits of a permanent establishment.

The move from EOR to an owned entity also requires planning. The hardest part is usually employment continuity. Employees need to leave one contract and sign another, while benefits, seniority logic, payroll timing, and local compliance are handled correctly. That is legal and operational work. It needs project management.

Provider choice changes the outcome

Cheap local support often becomes a black box

A single-market local provider can be the lowest upfront quote. It can also become a black box very quickly. The foreign parent does not know what it does not know in every jurisdiction, and some local firms use that information gap to incentivize dependency. The process becomes opaque, the scope expands quietly, and each step is often a surprise on what is next.

This is especially difficult for a finance team managing more than one country. Documents are stored locally. Notices arrive by mail. Instructions are received piecemeal by email or phone calls. Forecasting becomes difficult because the billing model is often hourly and the operating standard is reactive. The service may still be competent. The client experience is hard to control.

Big Four comfort comes with fragmentation

The default response to that uncertainty is often a Big Four firm. I understand the logic. It feels safer. I was part of the internal task force at Borderless AI that worked with a Big Four firm to set up the company's own entities globally. It was useful because it showed me the limits of that model very clearly.

The teams were fragmented by region. Each country required a different group, different handoffs, and repeated context-sharing from the parent company. The service was expensive and still rooted in email, PDFs, and local silos. The parent company effectively became the project manager while paying premium rates for the privilege. In many cases, the client is simply paying for that glut.

A better model for a mid-market company is centralized oversight with local execution. We have already moved a client with four global subsidiaries away from a Big Four provider by giving them clearer pricing, tighter visibility, and one place to manage the work. That is the operating standard I trust.

The operating model I trust

One system of record changes control

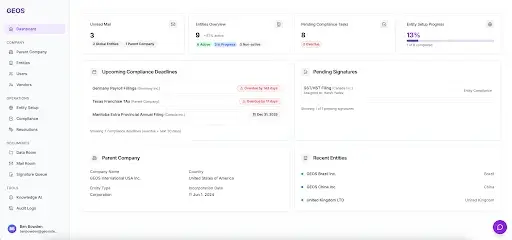

For a CFO, the real value is clarity. Entity data, key documents, local notices, deadlines, vendor responsibilities, and filing history should sit under one logo and one umbrella. Without that, managing a foreign footprint starts to feel like playing with a blindfold. The company may have vendors in place, but it does not have control.

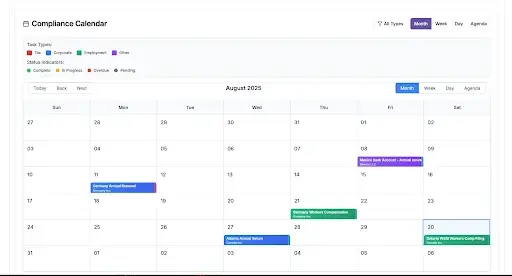

This is why we built GEOS around a centralized platform and service layer. We mapped the setup and management workflow across more than 80 countries because there are no shortcuts here. For Mexico, that means the filing steps, local document requirements, compliance calendar, and ongoing task ownership can be visible from the start. It also means local notices can be scanned, logged, and surfaced to the right internal team rather than disappearing into physical mail.

For finance teams, the operational improvement is straightforward. Critical notices can be tied to the entity record, tracked in a dashboard, and in some cases pushed into Slack rather than sitting in a local mailbox. That may sound simple. In global compliance, simple visibility is a major upgrade.

The model also needs to be vendor-agnostic. Real companies rarely replace every local provider at once. Sometimes the tax partner is working well and the legal partner is not. A platform should support both realities. It should also provide a scrutiny layer over local vendors, so the foreign parent is no longer putting blind trust into the local providers.

Technology still needs human execution

I am strongly in favor of technology in this space. I am not in favor of pretending that global entity work is fully automated. It is not. Incorporation, last mile tax filings, local payroll administration, and legal changes still require human execution in most countries, including Mexico.

That is also how I think about AI. At GEOS, Geovanna helps clients navigate information about their entity footprint and answer routine questions. It does not execute filings or make legal decisions. That boundary is intentional. Legal compliance does not tolerate hallucination, and local authorities still require human action.

The practical answer is a hybrid model. Use software to organize the work, track deadlines, store the documents, and create accountability. Fortify that with pre-vetted vendors and a client team that actually owns the process. That is how hidden risk becomes visible early, while it is still manageable.

Final view

Mexico can be an excellent place to build a long-term operating presence. It rewards companies that scope the project properly and respect the local realities. The risk usually starts when the work is framed too narrowly, the timeline excludes the intake and post-setup steps, or the provider model operates as if it is a black box.

Before I would approve a Mexico subsidiary, I would want clarity on the business objective, projected headcount, local revenue profile, legal representative, banking path, payroll design, and the owners for ongoing tax, accounting, and corporate secretarial work. If the company is transitioning from EOR, I would also want a clear employee transfer plan.

Mexico rewards process, visibility, and local execution that holds up after the incorporation certificate arrives. That is how I think about registering a subsidiary in Mexico without the hidden risks.

Frequently Asked Questions

What is the financial exposure of misclassifying Mexican contractors to delay entity setup?

Delaying setup by treating full-time workers as contractors is a massive control failure. Under Mexico's 2021 REPSE reform, violations trigger strict enforcement. One U.S. tech company recently faced a $2.5 million fine for misclassification. The math is simple: an EOR is far cheaper than funding a catastrophic compliance audit.

How should finance teams forecast mandatory employer payroll taxes in Mexico?

Statutory employer contributions will severely impact your OPEX if left unmodeled. According to local payroll guides, expect to add 25 to 35% to the gross salary. This includes mandatory housing fund (INFONAVIT) payments, which consume 5% of salary bimonthly. You must forecast these accruals precisely to prevent sudden budget overruns.

Why do newly registered Mexican subsidiaries frequently fail to execute their first payroll?

Banking and administrative bottlenecks often block execution. Mexico's social security institute (IMSS) authorizes only six banks to receive mandatory employer contributions. Furthermore, official systems still demand manual payment uploads via 3.5-inch floppy disk or USB. Without pre-vetted local banking rails, your legal entity remains a purely theoretical asset.

How can we establish vendor oversight without paying inflated Big Four advisory retainers?

Big Four firms operate in geographical silos, forcing your internal team to project manage via endless emails and PDFs. Instead, deploy a centralized system of record. By routing pre-vetted local partners through a single compliance dashboard, CFOs gain unified visibility, predictable pricing, and Slack-integrated alerts without the legacy consulting bloat.

Why do initial entity setup budgets often miss the true cost of operational readiness?

Law firms routinely quote a 2 to 4 week legal filing window, ignoring the expensive prerequisites. Every parent-company document requires certified Spanish translation, notarization, and apostille formalities before filing begins. Budgeting solely for the incorporation certificate leaves finance teams blind to the downstream costs of tax registrations and localized compliance.