For most CFOs, entity compliance becomes opaque the moment the company expands beyond its home market. Home-country finance, tax, and governance are familiar. Foreign annual filings, resident director rules, payroll registrations, and local notices are not. The result is predictable. Bills get paid, deadlines are assumed to be covered, and visibility falls away.

The pressure on finance teams is moving in the opposite direction. One report found that 96% of finance leaders expect increased technology spending over the next five years. The same report found that 59% have become more optimistic about AI’s potential to improve performance. At the same time, regulatory pressure is still rising. PwC reported that 77% of companies say compliance complexity has already hurt operations or growth. It also found that 71% plan to digitally transform compliance within the next three years.

This is not a niche problem. The largest multinationals now maintain over 370,000 subsidiaries globally. Even mid-market companies are building global footprints faster than the operating infrastructure around them.

My view on this is shaped by regulated industries. I have worked across healthcare, global payroll and EOR, and now foreign subsidiary setup and management at GEOS. The pattern is consistent. Complex systems fail when the workflow is opaque. They improve when each step is mapped, owned, and visible. That sounds simple. In this space, it is still uncommon.

At GEOS, we built the business around that point. We spent hundreds of hours mapping entity setup and ongoing management requirements across 80+ countries because there were no shortcuts. Technology only helps when the process itself has been understood first.

The process usually breaks in the same places

The broken entity compliance process is rarely a sign that finance has been careless. In most cases, the operating model is what is broken. It is fragmented, manual, and too dependent on providers who share information only when necessary. That creates cost leakage, forecasting problems, and avoidable risk.

The legacy firm problem

Large global firms still win a lot of business because they feel safe. That instinct is understandable. The brand is familiar. The team is large. The assumption is that a premium fee must produce premium control.

In practice, that logic breaks down quickly when the footprint covers several countries. These organizations are often fragmented by region. A company may sign with one global brand, but the work is still handled by separate country teams with separate workflows, separate contacts, and separate assumptions. The logo is centralized. The client experience is not.

I have seen this firsthand from the client side. The parent company ends up re-sharing documents, re-explaining the business case, and project managing multiple teams inside the same provider. The company is paying for scale, but it is not receiving the operating simplicity that should come with it. A large part of the fee is just overhead. Finance ends up paying for that glut.

I am not arguing that those firms provide no value. They can be safer than doing nothing, and they do have deep expertise. The issue is efficiency and visibility. Many of these models are bloated and stuck in the past. For a CFO trying to control risk and cost at the same time, that matters.

The local vendor black box

The cheapest local lawyer or accountant can look attractive at first. For one market and one immediate need, the quote may seem rational. Over time, this is often where the real damage starts.

Many single-market providers operate as if they are a black box. They do not share a full picture of what is required to set up and maintain an entity in their jurisdiction. Information is released in small pieces. The process is received piecemeal by email or phone calls. Each step is often a surprise on what is next. That increases the client’s dependency on the provider, especially when the provider bills hourly.

Once a company has entities in several countries, the overhead becomes significant. Someone internal has to manage invoices, signatures, deadlines, document requests, and follow-ups across all those markets. In my experience, that can become the equivalent of two or three full-time jobs. The hidden cost is rarely captured in the original sourcing decision.

I have seen the risk side of this as well. We have had to audit and remediate Latin American entities that came from a traditional provider with missing compliance documents and inactive nominee directors. The remediation work was extensive. It also should have been avoidable. The problem was not only the local provider. The larger issue was that no one had a proper scrutiny layer over the process.

The EOR overuse problem

EOR is different from entity management, and I think the category is often discussed too simplistically. I do not view EOR as a trap. I view it as a very useful tool at the right stage.

Every company has a global expansion journey that has a beginning, middle, and end. EOR is often the best option at the beginning. It is faster, lighter, and usually safer than hiring international workers as contractors while treating them like full-time employees. For a single hire or a small group, that trade-off often makes sense.

The economics change as headcount grows. Forming a local subsidiary often requires about $5,000 to $50,000 upfront before ongoing payroll, tax, and compliance costs are added. EOR providers generally charge $300 to $800 per employee per month. For one employee, EOR is usually more efficient. For a scaled local team, the equation changes quickly.

In my own work, I start to reassess the model once a company is carrying roughly 5 to 15 EOR employees in one country, depending on how difficult that market is. In the UK or Canada, direct setup can make sense much earlier, often around 3 to 6 employees. In more complex jurisdictions like France or Belgium, the break-even can be much later.

The compliance side matters just as much as the cost side. Once a company is materially scaled through EOR in one country, permanent establishment risk deserves direct attention. An unsavory exit can bring local scrutiny to the parent company, even if an EOR sits between the parties contractually. EOR firms do not absorb all liability. In many cases the risk is shared.

Forecasting fails when the timeline is incomplete

One of the most common problems in entity work is that timelines are wrongfully quoted almost every time. The quoted timeline often reflects only the narrow government processing period after an application is lodged. It does not reflect the actual path from decision to operational entity.

Incorporated is not operational

For finance, the difference between “incorporated” and “operational” is critical. An entity may legally exist, but still lack tax registrations, payroll access, social security setup, banking, and the practical ability to employ or contract. Many teams do not realize this until they are already inside the process.

The unglamorous steps are what usually drive the real timeline. Parent company documents have to be collected. Director and UBO information has to be gathered. Documents may need to be notarized, apostilled, translated, and couriered. Some countries require local notary appointments. Others create issues around foreign bank KYB for share capital deposits. In some markets, the bank process is harder than the incorporation itself.

I have seen applications expire because a director or owner was slow to provide notarized identification or proof of address. Once that happens, the process can restart from scratch. That delay is not necessarily the provider’s fault, but it still affects the forecast. A realistic model has to account for it.

This is one reason I prefer very explicit scoping. In the UK, the incorporation step itself can often be completed in one to two weeks. In many other countries, four months is more realistic for the setup process, and the full path to a functioning entity can extend beyond that. A Toku analysis places typical entity formation at two to six months, while EOR hiring can often happen in days or weeks after contracts are signed. That speed gap is real. It should be evaluated honestly, not hidden behind a headline quote.

Corporate secretarial support still looks outdated

The same issue exists after incorporation. In many countries, corporate secretarial support still means physical mail, scattered emails, and PDFs. The role is there to keep the lights on from a compliance perspective, but the delivery model is still operating with 1990s assumptions.

For a CFO, that creates a familiar problem. Notices arrive late. Annual obligations are tracked in someone’s inbox. Local partners hold the documents. Internal teams do not know what has been filed, what is due next, or whether the work has actually been completed. The process becomes difficult to audit and even harder to forecast.

That is why I believe entity compliance needs to be treated as an operating system, not a series of vendor interactions.

What a healthy entity compliance process looks like in 2026

A strong process in 2026 is built around visibility, modular control, and realistic human execution. In my view, the best setups function as an act of mutual problem solving between finance, operations, local experts, and the provider coordinating the work.

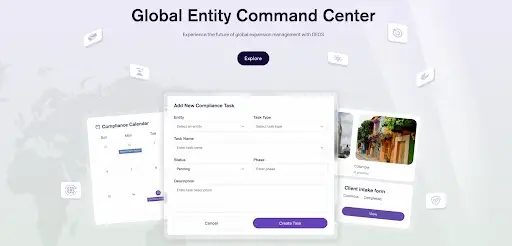

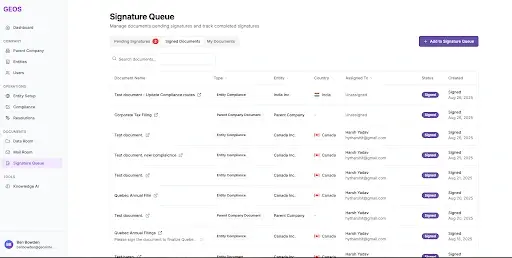

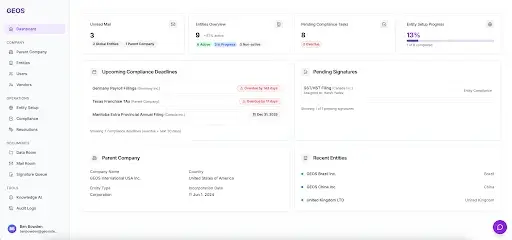

Start with one system of record

Every entity should sit inside a clear system of record. That system should hold the core legal attributes of the entity, its ownership and structure, its directors, registered address, key constitutional documents, annual obligations, tax and payroll registrations, vendor relationships, and an audit trail of actions taken. It also needs named ownership over each compliance task and clear due dates.

Without that layer, finance is effectively playing with a blindfold. Information comes from different directions, but no one sees the full court. That is manageable with one foreign entity. It becomes risky with five or 10.

This is the problem we designed GEOS to solve. The goal was never to eliminate local experts. The goal was to organize the entire process around one visible workflow and one centralized record. That is also why notifications matter so much. The “aha” moment for many finance teams is very simple: foreign notices and deadlines stop living in the mail and start appearing inside a platform, with the option to route them into Slack or other internal systems.

Apply the right control model by country

One of the biggest mistakes I see is treating every market the same. That creates overspend in some countries and under-management in others. A company may have one entity that only needs a lightweight system of record and another that requires full CorpSec support, ongoing annual filings, resident director management, and coordination across tax, payroll, and legal vendors.

I strongly prefer modularity. At GEOS, we price the platform on a per-entity basis for exactly that reason. The Access layer starts at $49 per entity per month for system-of-record visibility, and the higher-touch service layers are quoted by country based on what the entity actually needs. The broader point is not the number. It is the structure. Finance should be able to deploy the right level of control where it is needed, rather than overbuying a global retainer.

A vendor-agnostic model is also important. Some companies already have a solid local provider in one country and a failing one in another. Replacing all vendors at once is unnecessary. A better approach is to bring those partners into one operating layer, compare their work against a pre-mapped compliance baseline, and then decide where replacement makes sense. That scrutiny layer is where a lot of risk reduction actually happens.

Resident director support is a good example. In markets where that role is mandatory, the decision should not be treated as a simple admin step. That individual is taking personal legal liability. Vetting matters, and so does the process for ongoing oversight.

Use AI for speed, not for false confidence

AI has a role in this category, but it needs very clear guardrails. Finance teams are right to be more optimistic about AI where it improves visibility and response time. They should be cautious wherever it creates false confidence.

At GEOS, Geovanna is intentionally restricted from executing actual incorporation or compliance tasks. That is a deliberate design choice. Many countries still require manual, physical, or highly localized steps. An AI agent cannot attend a public notary process in the Netherlands, explain a foreign company’s purpose, submit physical documentation, or safely navigate every local government portal. The legal safety simply is not there.

Where AI is useful is immediate retrieval of verified information. It can answer questions about a company’s entity footprint, registrations, documents, and high-level obligations. It can help users navigate the platform faster and then hand off to the account team when human execution is required. That is a practical use of AI. It improves speed without pretending that compliance has become fully autonomous.

Re-underwrite every EOR market

The finance case for moving from EOR to owned entities should be reviewed regularly, country by country. The wrong way to approach it is as a one-time strategic decision. The right way is to reassess as headcount, local revenue, and operating needs change.

The first-year comparison will often favor EOR at low headcount. A Toku analysis estimates that a single hire through EOR may cost roughly $6,000 to $18,000 per year in service fees, while the first year of setting up and running a local entity can be materially higher. That is exactly why EOR exists.

The balance changes once a local team reaches critical mass. At that point, the savings from eliminating per-employee fees become meaningful. So do the operational benefits. The company gains more control over benefits design, HR policy, equity administration, and local contracting. In some markets, direct presence also helps with enterprise or government sales.

The actual transition requires discipline. In practice, I think about it in four connected phases: entity setup, employment infrastructure, transfer planning with the EOR, and then a clean HR playbook for the new entity. The hardest part is usually legal continuity for employees moving from one contract to another. Seniority, benefits, vacation accruals, payroll timing, and communications all need careful coordination.

How I would reset a broken process now

If I were assessing a broken entity compliance process in 2026, I would start with a full inventory of the current footprint. That means every entity, every EOR country, every registered address, every resident director arrangement, every tax registration, every payroll provider, and every local legal or accounting partner. I would also ask one simple question immediately: where do the documents actually live?

The second step would be to map recurring obligations country by country. For each entity, I would want a clear baseline of annual filings, registrations, deadlines, and ownership. I would compare that baseline against what current providers are actually doing. This is also the point where partner performance should be reviewed directly. Is the vendor responsive? Is the pricing predictable? Are surprises becoming normal? If the answer is no, change should happen early.

The third step would be a fresh economic review of every EOR market and every proposed new entity. I strongly prefer a phased approach. Some companies should stay on EOR. Some should test a market with local sales activity below the threshold that creates more complex obligations. Some should move to direct entities immediately because they have multiple business reasons to do so. Good advice has to meet companies where they are.

The final step is centralization. Documents, tasks, notices, and vendor interactions need to sit inside one visible operating layer. Human communication should still exist through standing meetings, Slack channels, and direct support. The platform should organize the work, not replace accountability.

I also prefer speed over theoretical perfection. A B-plus plan executed today is better than an A-plus plan executed next week. The same applies here. A clean audit and a clear system of record solve more risk than another quarter of fragmented emails.

One final point matters internally. If finance, legal, or operations teams are surprised later when controls tighten, that is usually a failure of leadership and communication. The expectations, the risks, and the economic logic should be clear early.

Closing

Entity compliance in 2026 is an operating discipline. It requires realistic timelines, a centralized system of record, modular vendor oversight, and clear boundaries around what technology can and cannot do. Companies that continue to run this process through fragmented vendors, physical mail, and scattered PDFs will keep absorbing unnecessary cost and risk.

I co-founded GEOS because I believed this model needed some refreshment. The industry did not need more opacity. It needed a better way to map the process, coordinate local experts, and give finance teams real visibility without forcing them into Big 4 overhead or local black boxes.

The process is fixable. It becomes manageable once every step is visible, every task has ownership, and every market is evaluated on its own terms. That is the standard I believe CFOs should expect in 2026.

Frequently Asked Questions

How do we calculate the exact ROI of transitioning from an EOR to an owned entity?

Calculate your localized headcount against the $300 – $800 per employee per month EOR fee. In simple markets like the UK, breakeven is around 3 employees. Compare this ongoing bleed against the one-time $1,000 to $15,000 setup cost. The mathematical ROI at critical mass is undeniable.

Does an EOR completely shield our parent company from foreign compliance liability?

No. EORs are a useful bridge, but they do not absorb all liability. If you scale heavily, permanent establishment risk attaches to the parent. As regulatory scrutiny tightens – which 77% of companies say hurts growth – you need direct, visible control over your legal footprint.

How do we migrate existing local accountants onto a centralized compliance platform?

You do not need to fire performing vendors. A mature compliance engine operates as a vendor-agnostic oversight layer. You bring existing partners into a single system of record to enforce strict scrutiny and map deliverables against a baseline, eliminating the single-market black box entirely.

Why shouldn’t we rely on Big 4 firms to handle our global entity compliance?

Big 4 firms offer safety but at severe premiums. As multinationals manage over 370,000 subsidiaries globally, relying on legacy conglomerates often yields a fragmented workflow. You pay for overhead, but still suffer from opaque, localized execution without centralized technological visibility.

How does a centralized operating system prevent hidden costs in entity management?

Opaque workflows create cost leakage. By mapping recurring obligations into a single dashboard, you eliminate surprise billable hours and late penalties. With 96% of finance leaders planning tech investments, consolidating this data is the definitive way to enforce vendor accountability and protect forecasts.